The flip side however, is that this massive acceleration in demand challenges production capacities, supply chains and job market flexibility. Shortages and scarcity are becoming visible in many areas of the economy, from computer chips to building materials, labor to transport capacity. This is driving prices higher and reigniting inflationary concerns. After being warmly welcomed last year as a way to dampen an historical collapse in economic activity, ultra-supportive monetary and fiscal policies are increasingly seen as driving a possible overheating that may threaten future economic stability. Central bankers and governments, while wary of removing support too soon, are now looking toward the next step that will be the withdrawal of the exceptional pandemic-related policies. As such, the peak in central bank and government support is most likely now behind us.

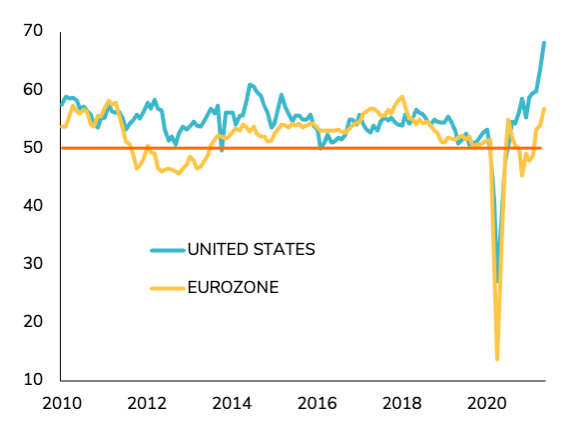

In parallel, the peak ineconomicgrowth has probablyalready been reached in the US. We cannot reasonably expect a continuation of the breakneck pace of improvement seen since the beginning of the year. Maintaining the current economic growth rate in the US would already be very positive in this environment.

The rest of the world is not there yet. Europe is still in the “acceleration” phase, thanks to the easing of pandemic restrictions and vaccine roll-outs, and this will drive global momentum in the coming months. Some large emerging economies face an unpleasant combination of Covid-19 resurgence and accelerating inflation, and are lagging in the positive global economic cycle.