Positive economic momentum, combined with super low nominal rates and central bank liquidity injections, create an environment where everyone is looking to invest into assets that will provide positive nominal, and ideally, positive real income over the next two to three years. As government rates will remain low in nominal and negative in real terms as well, the great hunt for yield continues apace.

While credit offers some yield in absolute terms, this is less attractive than three months ago. In relative terms, the equity market looks more attractive. But investors need to be selective and find companies which will still be posting positive activity and revenues in several years, in an industry that will not fall into post-Covid obsolescence. The downside is that some areas of the equity market will become victims of their own success. Investors need to be very careful about what they are prepared to pay in the post-Covid world.

Broadly, the trends of the past few months remain in place, with valuations in the tech, consumer and healthcare sectors still rising. Meanwhile, sectors acutely impacted by Covid are still suffering. If a vaccine is made available, the catch-up potential for these under-performing sectors, such as hotels, travel and leisure, will be quick and very large. We are monitoring the risk of sectorial rotation, but believe it is still too early to position for this.

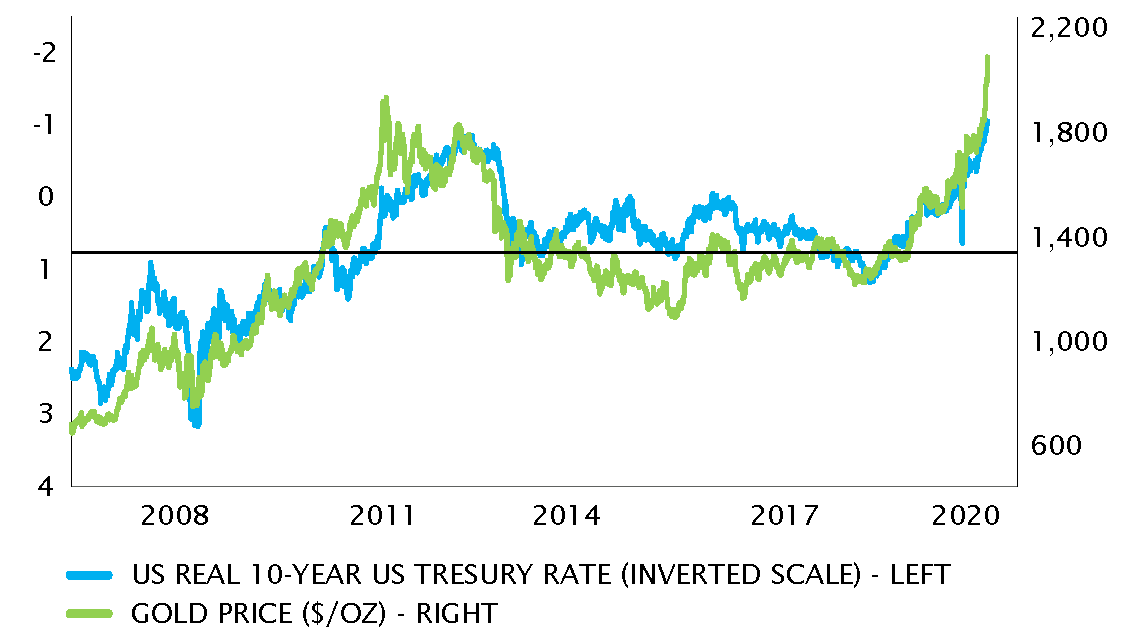

Inflation linked bonds continue to be attractive compared to nominal government bonds with the decline in real rates. Recently, the inverse correlation between gold and real rates has been particularly strong. In fact, the latest acceleration shows gold is moving ahead of real rates, anticipating further falls. This is related to central bank attitudes to inflation, with the Fed conducting a review of its inflation strategy.

Currently, the Fed has a dual mandate – to target the lowest level of unemployment, and stability in prices. In the past few years, sustained low inflation has raised questions around this framework and the set 2% target, which was responsible for rate hikes and the end of QE. In September, the Fed is expected to announce a new average inflation target, which aims for an average of 2% over several years. This means if inflation rises above 2% after two years at 1%, the bank would leave it unchanged until inflation averages out to 2% over the period.

This supports speculation on gold prices, as real rates could be allowed to fall further. Given gold has no fundamental value, we would not be surprised to see prices rise further – by as much as 10 percent or even higher.