Within the Japan-style scenario, market cycles still occur, but the episodes are typically milder and shorter. For example, risk assets rose off the back of very accommodative central banks and synchronised global growth in 2017, before being dragged back down by the Federal Reserve reversal on monetary policy. Similarly, we believe that the global economy will experience a positive mini-reflationary cycle in the coming months – and investors need a tactical response to capitalise on it before it fades away

Asset Allocation Insights

Vaccine delivers a shot-in-the-arm for risk assets

Tuesday, 12/01/2020Although the global economy remains mired in a ‘Japanification’ scenario – the prevailing state of lower rates and slower growth – positive news of a Covid-19 vaccine was a boost for risk assets. In the short-term, this could trigger an acceleration in both growth and inflation (reflation). If this materialises, investors should capitalise on the temporary shift, before we return to the deeper, more profound de- flationary cycle.

Adrien Pichoud

Chief Economist & Senior Portfolio Manager

Fabrice Gorin

Senior Portfolio Manager

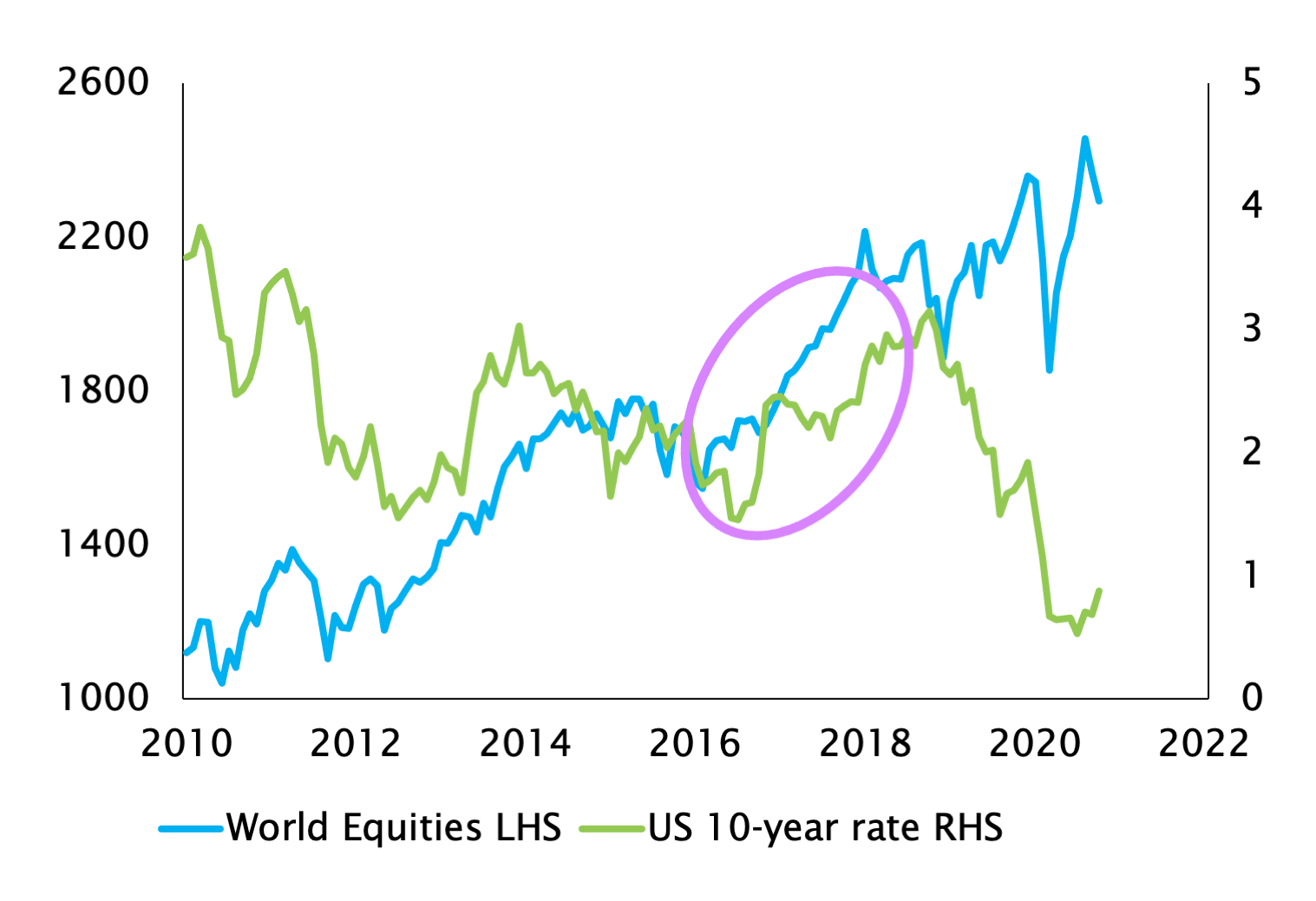

TOWARD A MINI-REFLATION CYCLE “À LA 2016-17” IN 2021, WITH RISING EQUITIES AND RATES?

GLOBAL EQUITIES AND US TREASURY 10-YEAR RATE

GLOBAL EQUITIES AND US TREASURY 10-YEAR RATE

Source

BANQUE SYZ, FACTSET

Reflation requires coordinated global growth and a supportive policy environment. As optimism around a post-Covid return to normal sweeps through markets and economic data adjusts accordingly, we expect these conditions to transpire over the next six months. However, evaluating the impact of the second wave of Covid-19 will be crucial before we can be sure of a reflation.

Flexible in fixed income

Acknowledging the rising possibility of a reflation, we have tactically increased risk exposure through our fixed income allocation. We have reinforced our bias to hard currency emerging market debt, which has lagged the credit recovery so far. Spreads are attractive compared to the broader market and emerging market assets should benefit from a reflation scenario. A combination of global growth, higher risk appetite and a softer dollar is the sweet spot for emerging market debt.

In addition, to counter the rising probability of interest rate increases and steepening yield curves in a global growth environment, we have further reduced duration in the portfolios. We did this by selling long-dated positions, notably US treasuries, as the US curve appears most prone to a bear steepening. We also took some profits on long-dated corporate bonds, as valuations become less appealing.

However, credit remains attractive compared to cash and government bonds in the risk-on environment, and we have implemented hedges that allow us to maintain some exposure to credit spreads while containing the impact of a potential rise in rates. We still have a mild preference for high yield, with attractive valuations, but the deterioration in credit fundamentals warrants remaining selective.

By reacting to shifts in economic dynamics through tactical moves like these – taking advantage of expected mini-cycles in asset prices – we are able to generate positive performance despite the low rate environment – even on negative yielding assets. Dynamic asset allocation and tactical positioning are key for navigating the current environment of very low rates, as this allows us to capitalise on even the shortest and mildest of reflationary cycles.

Dynamic approach to equities

On the equities side, we are also preparing to make strategic adjustments. Given our conviction we will ultimately return to a Japan-like scenario, we do not believe value can sustainably outperform growth. However, if the impact of the second wave of Covid-19 is relatively mild and coordinated global growth is reignited, there will be an opportunity to tactically increase our cyclical exposure in the short term to drive alpha within the portfolios.

While our portfolios have a growth bias, we also have some cyclicality in the equity allocation – so we will not be wrong- footed if a rotation materialises early. Our overweight to quality companies includes some industrial names and other more cyclical stocks. If we see confirmation of positive global growth, we will look to increase cyclicality in the portfolios in the short term. Core eurozone equity markets, such as France and Germany, are particularly attractive given the super-low rate context in Europe.

Meanwhile, structurally, we are increasing our exposure to emerging markets – specifically China, as we see long-term potential for the country to catch up to developed market peers. Chinese equities, which have lagged for the last five years, are currently benefiting from the low-rate environment and global growth pickup, in addition to the authoritarian government’s handling of the Covid-19 pandemic. The country has not witnessed a second wave of infections, and liquidity injections and fiscal support have boosted domestic credit growth. We are playing this through a combination of ETFs, to provide us with exposure to Hong Kong listed giants, such as Alibaba and JD.com, as well as domestic A-shares, which are less dependent on the foreign environment.

Within the Japanification framework, reflationary episodes will occur. While these events will create short-term volatility, they also provide valuable windows for multi-asset portfolio managers to dynamically deliver additional alpha. At SYZ, we embrace these opportunities to demonstrate the value of active management.

Disclaimer

This marketing document has been issued by Bank Syz Ltd. It is not intended for distribution to, publication, provision or use by individuals or legal entities that are citizens of or reside in a state, country or jurisdiction in which applicable laws and regulations prohibit its distribution, publication, provision or use. It is not directed to any person or entity to whom it would be illegal to send such marketing material. This document is intended for informational purposes only and should not be construed as an offer, solicitation or recommendation for the subscription, purchase, sale or safekeeping of any security or financial instrument or for the engagement in any other transaction, as the provision of any investment advice or service, or as a contractual document. Nothing in this document constitutes an investment, legal, tax or accounting advice or a representation that any investment or strategy is suitable or appropriate for an investor's particular and individual circumstances, nor does it constitute a personalized investment advice for any investor. This document reflects the information, opinions and comments of Bank Syz Ltd. as of the date of its publication, which are subject to change without notice. The opinions and comments of the authors in this document reflect their current views and may not coincide with those of other Syz Group entities or third parties, which may have reached different conclusions. The market valuations, terms and calculations contained herein are estimates only. The information provided comes from sources deemed reliable, but Bank Syz Ltd. does not guarantee its completeness, accuracy, reliability and actuality. Past performance gives no indication of nor guarantees current or future results. Bank Syz Ltd. accepts no liability for any loss arising from the use of this document. (6)