While the rise of passives presents a challenge, true active managers should not fixate on the mounting forces of beta, and, instead, focus on delivering value for investors.

The passive era had a singular moment of inception. In 1975, John C. Bogle, founder of Vanguard, inspired by a research article published in 1974 by the Nobel Prize-winning economist Paul Samuelson, revolutionized the world of finance by creating the management of automatic market steering without an active manager.

Since then, the rise of passive investment vehicles has been a force for positive change: a natural evolution forged through greater innovation and heightened scrutiny around fees and charges. Passives have offered cost-effective stock market exposure and greater access to more esoteric asset classes. But perhaps their greatest legacy will be the democratisation of the investment world – which is allowing a greater number of smaller investors to enter the market via emerging ‘robo-investing’ brokers.

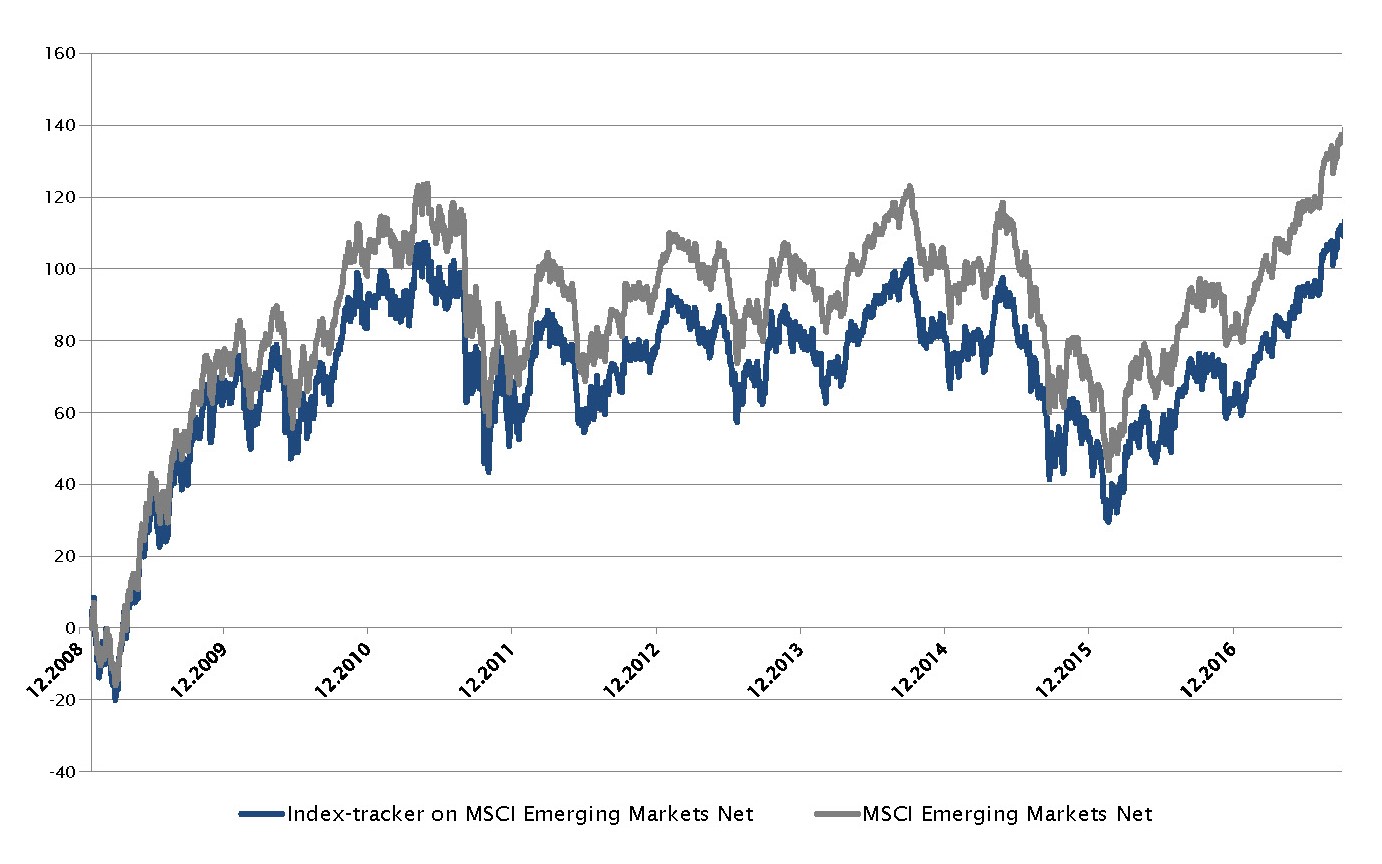

And now, more than forty years since their introduction, increasingly data is highlighting how passives have outperformed the vast majority of actively managed funds. This raises the question of the appropriateness of management fees, especially in times of sluggish growth and ultra-low rates. Never before has the scrutiny been greater on the active world. Now is the defining hour when active management must demonstrate its value.