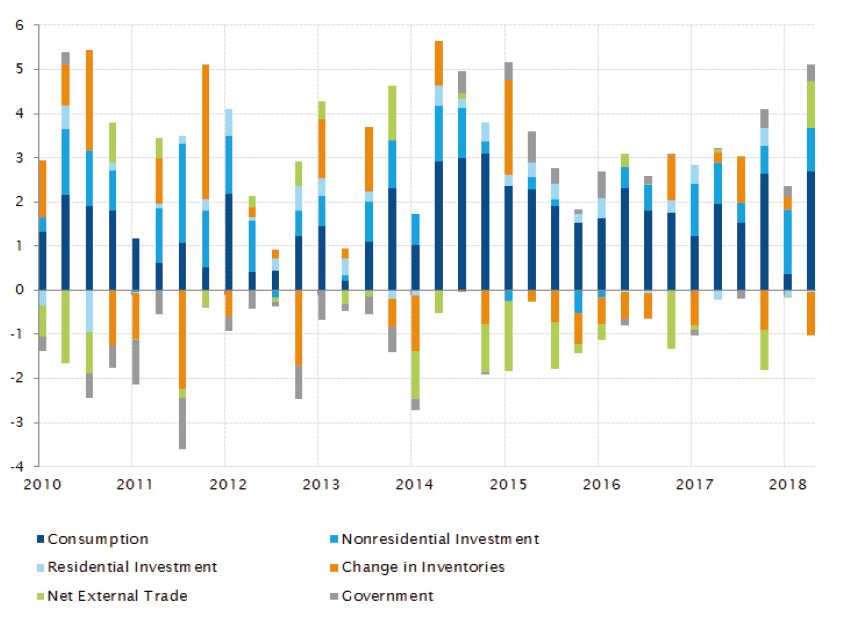

- 1. US - GDP growth momentum continues

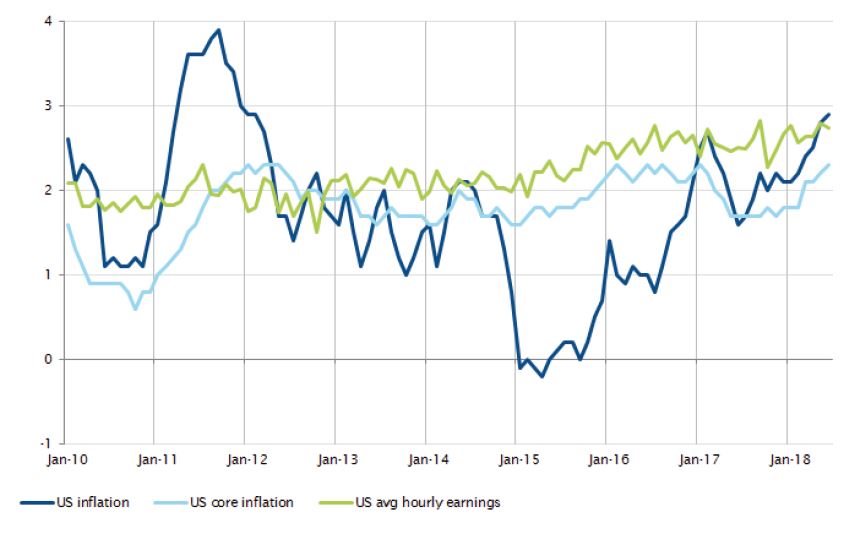

- 2. US - inflation is approaching peak

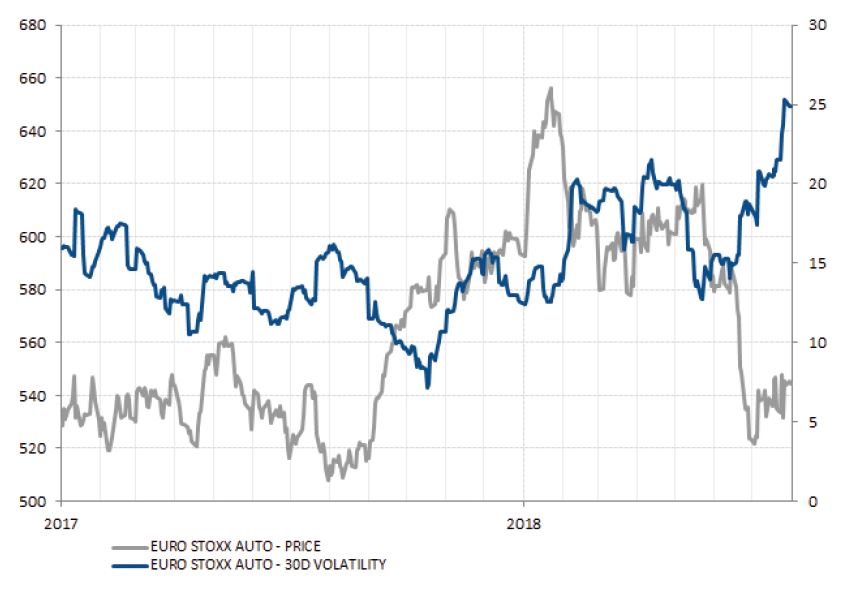

- 3. Equity - European auto stocks remain volatile after earnings results and political de-escalation

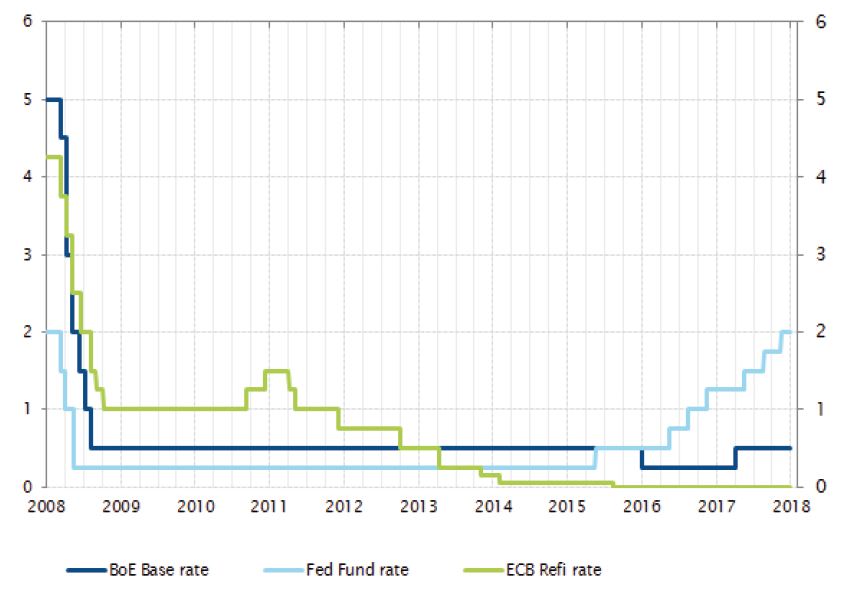

- 4. UK - BoE raises rates for the second time in ten years

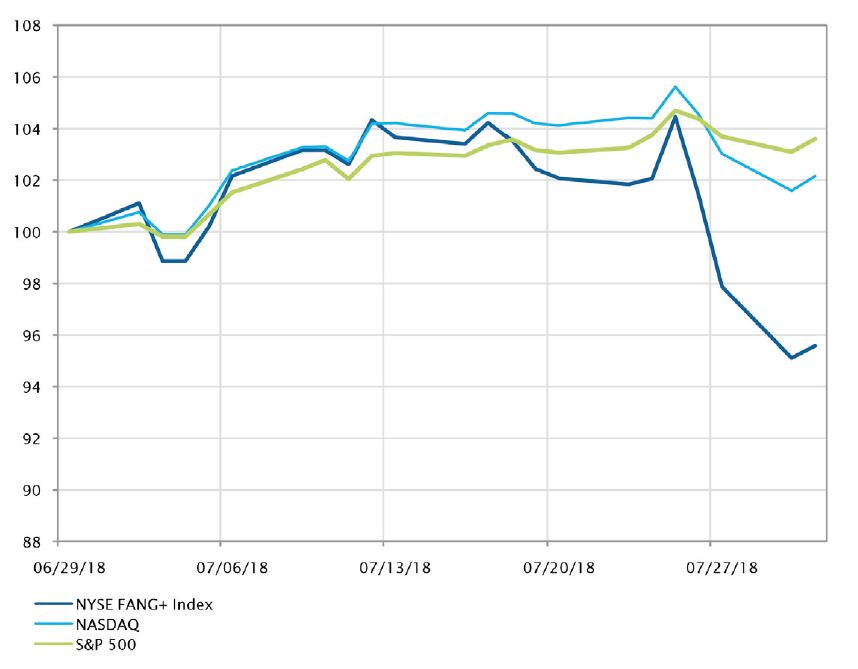

- 5. Equity – major US tech companies under pressure following earnings announcement

US - GDP growth momentum continues

US GDP growth stayed strong in Q2, rising at 4.1% qoq, the highest pace since 2014. While this was just shy of growth expectations, which stand at 4.2%, both consumer spending (4.0%) and business investment (7.3%) beat consensus estimates. Consumer spending strongly rebounded after a weak print in Q1, which was revised down at 0.5%. The decline in inventories was the weak spot, subtracting 1.1% from growth - the most since 2014.

It is worth mentioning the personal savings rate was upwardly revised from 3.3% to 7.3% in Q1 and reported at 6.8% in Q2. This revision indicates the momentum in consumption is more robust than expected.

Robust growth due to strong domestic demand

Source: SYZ Asset Management, BEA, Factset. Data as at : 31 July 2018

US inflation is approaching peak

Source: SYZ Asset Management, Factset. Data as at : 31 July 2018

US - inflation is approaching peak

US inflation continued to drift higher, with headline CPI hitting a six-year high at 2.9% in June. However, short-term dynamics suggest the peak is near for yearly inflation. Higher oil prices - which rose by over 50% in the last 12 months - explain part of the movement, but underlying core inflation is also gradually increasing, fuelled by rising wages. So far, this increase in inflation is no surprise and indeed welcomed by the Fed, as it justifies the ongoing gradual rate hike cycle.

In the rest of developed economies, the story is somewhat different. On top of the upward pressures stemming from higher energy prices, recent currency movements have also had a temporary impact, cushioning or exacerbating the contribution of oil prices to headline inflation. Currency moves may also influence core inflation, especially in small open economies such as Switzerland, but the real driver, wage growth, remains anaemic.

Equity - European auto stocks remain volatile after earnings results and political de-escalation

European automakers experienced another eventful month, with 30-day average volatility reaching 25%. Disappointing margin forecasts for the auto-parts maker Faurecia, down 7%, started the month off on the wrong foot, followed by Fiat Chrysler’s cut to its revenue and profits forecast, due to disappointing sales in China. In the meantime, Peugeot posted strong results, surging to a seven-year high of 15% as Opel returns to profit, which pushed the whole sector up. Finally, the strongest positive catalyst was President Trump’s announcement he will hold off on new auto tariffs, after a meeting with European Commission President Juncker. Over the month, the Euro Stoxx 600 Automobiles & Parts gained 4.0%, outperforming the broad index - the Eurostoxx 600 rose by 3.1%.

Volatility gauge is increasing

Source: SYZ Asset Management, Bloomberg. Data as at : 31 July 2018

The BoE hikes interest rates despite ongoing Brexit uncertainty

Sources : Bloomberg, SYZ Asset Management. Data as at : 31 July 2018

UK - BoE raises rates for the second time in ten years

Although the United Kingdom is mired in uncertainty around Brexit negotiations, the Bank of England maintained its stance and raised rates by 25bps to 75bps. This was no surprise as the market was anticipating this hike. The Bank highlighted economic activity in Q2 was solid and consumer confidence good. Overall, the Bank of England’s statement was similar to the last one, with very few changes.

Higher interest rates are a sign the Bank of England thinks the economy can sustain a rate rise, even if some data has shown softness of late. It will be interesting to watch the next set of consumer and business confidence figures to see how Brexit developments can impact the economy.

Equity – major US tech companies under pressure following earnings announcement

In the United States, July was a difficult month for the technology sector, particularly for the FANG index - composed of Facebook, Amazon, Netflix and Alphabet - which lost 4.4% MTD, compared to the NASDAQ and the S&P 500, which gained 2.2% and 3.7% respectively.

Disappointments in the FANG second quarter earnings were severely sanctioned by markets. Facebook, for example, lost 19.0% on the day following its poor results, which were due to slowing advertising sales growth and users. Twitter went down 20.5% as the number of monthly active users fell by one million and Intel lost 8.6%.

In the case of Facebook, this single day fall represents a loss in the company’s market cap of circa $119.4bn, the largest decline in value of a listed US company - equalling the sum of the twenty smallest S&P 500 companies by market cap.

Finally, the S&P 500 Information Technology index lost more than 5% since Facebook reported its earnings on 25 July.

NYSE FANG+, NASDAQ and S&P 500 indices evolution in June (rebased at 100)

Sources : Bloomberg, SYZ Asset Management. Data as at : 1 August 2018

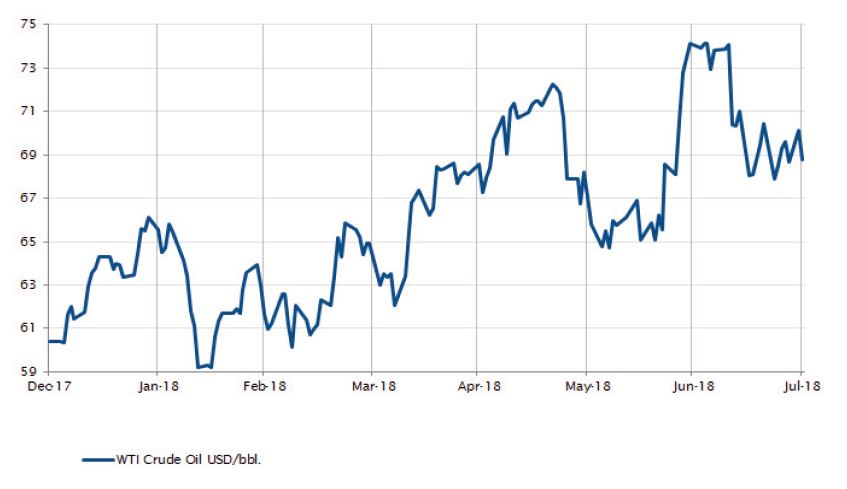

WTI Crude Oil price evolution (USD/bbl.)

Sources : Bloomberg, SYZ Asset Management. Data as at : 2 August 2018

Commodities – oil price under pressure

Oil prices saw the worst monthly drop in the last two years following worries around demand and supply, a weakening outlook for global growth and ongoing US-China trade tensions.

The possibility disruption in Libya will come to an end, while Iran exports are falling slower than planned, is putting even more downside pressure on the oil price.

In parallel, OPEC and Russia are raising their production levels and US crude inventories are creeping up - producing 3.8 mn barrels at the end of July compared to a Bloomberg forecast of a 3.0 mn barrel decline.

Finally, Saudi production in July increased by 230,000 bbl/d to reach 10.65 mn bbl/d and total OPEC production increased by 300,000 bbl/d in the last month.

In this context, Brent and WTI finished the month of July respectively down 6.5% and 7.3% at 74.25 USD/ bbl and 68.7 USD/bbl.

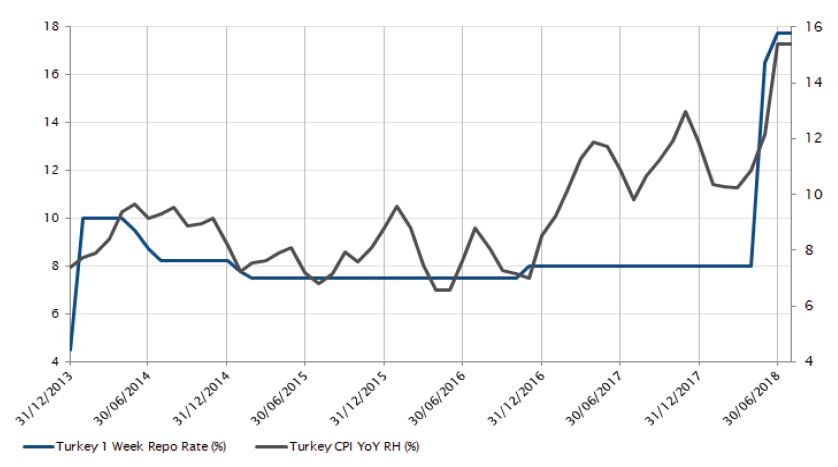

Turkey – no rates hike for the Turkish central bank

The Central Bank of Turkey (CBT) once again surprised markets by not hiking rates in July.

The inflation trajectory is still on a deteriorating path and the CBT defended its position, saying it was adopting a ‘wait and see’ approach, anticipating a potential delayed disinflation impact.

This confirmed investors’ scepticism regarding the CBT’s independence and President Erdogan’s recent amendment of the law granting him more control over the central bank.

More recently, the CBT recognised it will not meet its 5% inflation target in the next three years. This news also came as a major disappointment to investors awaiting monetary policy tightening.

On the other hand, Erdogan still emphasises he wants lower interest rates and monetary policy easing to stimulate the economy, which could add further inflationary pressures.

In this context, the lira was down 6.6% against the US dollar in July, while the Turkish 10-year government bond yield spiked at 18.0% - up 188bps from the end of June.

Turkey: Central Bank rate and inflation (%)

Sources : Bloomberg, SYZ Asset Management. Data as at : 2 August 2018

Rising inflation despite record-high interest rates

Sources : Bloomberg, SYZ Asset Management. Data as at : 31 July 2018

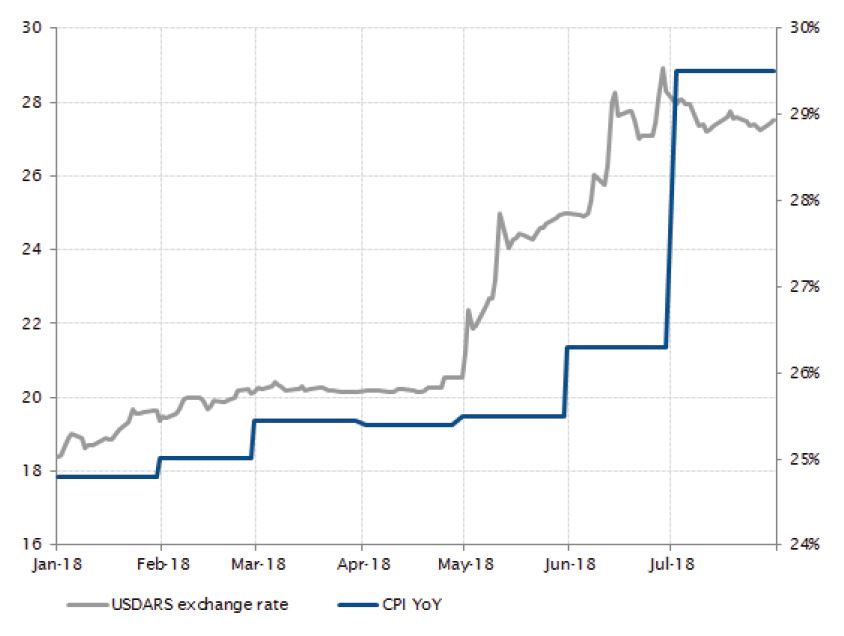

Argentina - inflation is getting out of hand

Argentina’s President Mauricio Macri recently admitted the country’s annual inflation rate might reach 30% in 2018. When the president took office in 2015, his main task and goal was to reboot the economy and cut inflation.

Unfortunately, the country had to request a $50bn credit line from the IMF, with high borrowing costs, and the stock market plunged. Foreign investors turned away from Argentina, regarding the environment as hostile due to high inflation. However, for investors willing to take high risks, very high interest rates could be extremely rewarding if inflation starts to cool off from current levels. The issue President Macri now faces is to maintain a good approval rating in order to put his plan into action to get the country back on track.

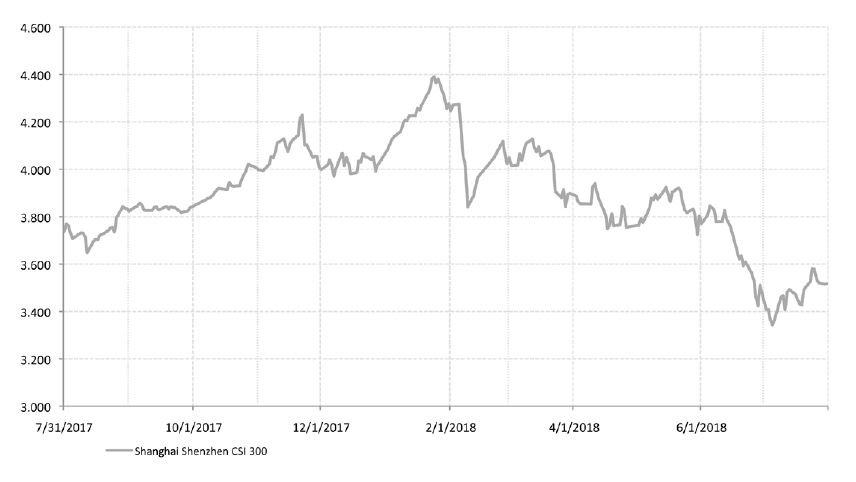

China enters a new easing phase

Chinese authorities unveiled a set of fiscal measures to boost the economy. Escalating trade tensions provided the pretext for this policy shift, but the Chinese economy was slowing amid attempts to restrain credit growth. The State Council announced fiscal stimulus via corporate tax cuts and infrastructure spending. In addition, the People’s Bank of China unexpectedly injected $74bn of liquidity into financial institutions via the MLF (medium-term lending facility). These measures do not constitute a U-turn towards significant easing but rather a recalibration offsetting some drag from the deleveraging campaign. The stimulus could take some time to spill over to the economy but the effect on equity markets was immediate. Chinese stocks recovered losses from early July, ending the month flat.

Chinese equities recovered due to new easing measures

Sources : Bloomberg, SYZ Asset Management. Data as at : 31 July 2018

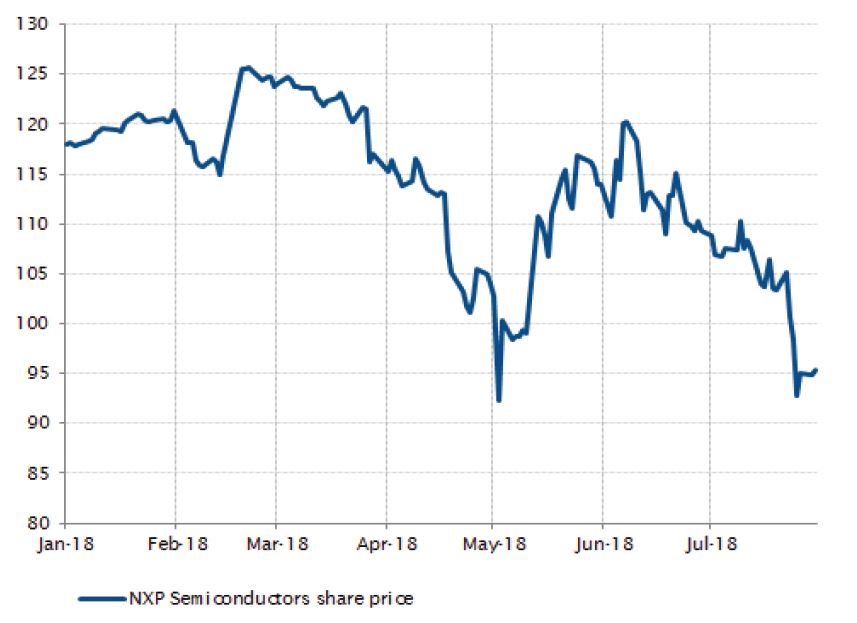

NXP Semiconductor plunged after the deal collapsed

Sources : Bloomberg, SYZ Asset Management. Data as at : 31 July 2018

Merger: Qualcomm/ NXPI deal: trade war victim?

July marked the end of an almost two year saga in the US semi-conductor space, the acquisition of NXPI by its rival Qualcomm. The transaction, which was valued at approximately $44bn, was one of this year’s major merger transactions. The deal obtained regulatory approval from all required authorities except the Chinese anti-trust office, MOFCOM. Due to ongoing trade tensions and aggressive rhetoric between the US and China, markets started to doubt MOFCOM would grant its approval and the transaction’s success became uncertain.

Finally, Qualcomm walked away from the deal before the deadline when it became clear China would not grant its approval, following NXPI’s announcement of a %5bn share buyback plan. A few days later, MOFCOM approved another deal, a European one, probably a sign the QCOM/NXPI decision was more political than economic.

Disclaimer

This marketing document has been issued by Bank Syz Ltd. It is not intended for distribution to, publication, provision or use by individuals or legal entities that are citizens of or reside in a state, country or jurisdiction in which applicable laws and regulations prohibit its distribution, publication, provision or use. It is not directed to any person or entity to whom it would be illegal to send such marketing material. This document is intended for informational purposes only and should not be construed as an offer, solicitation or recommendation for the subscription, purchase, sale or safekeeping of any security or financial instrument or for the engagement in any other transaction, as the provision of any investment advice or service, or as a contractual document. Nothing in this document constitutes an investment, legal, tax or accounting advice or a representation that any investment or strategy is suitable or appropriate for an investor's particular and individual circumstances, nor does it constitute a personalized investment advice for any investor. This document reflects the information, opinions and comments of Bank Syz Ltd. as of the date of its publication, which are subject to change without notice. The opinions and comments of the authors in this document reflect their current views and may not coincide with those of other Syz Group entities or third parties, which may have reached different conclusions. The market valuations, terms and calculations contained herein are estimates only. The information provided comes from sources deemed reliable, but Bank Syz Ltd. does not guarantee its completeness, accuracy, reliability and actuality. Past performance gives no indication of nor guarantees current or future results. Bank Syz Ltd. accepts no liability for any loss arising from the use of this document. (6)