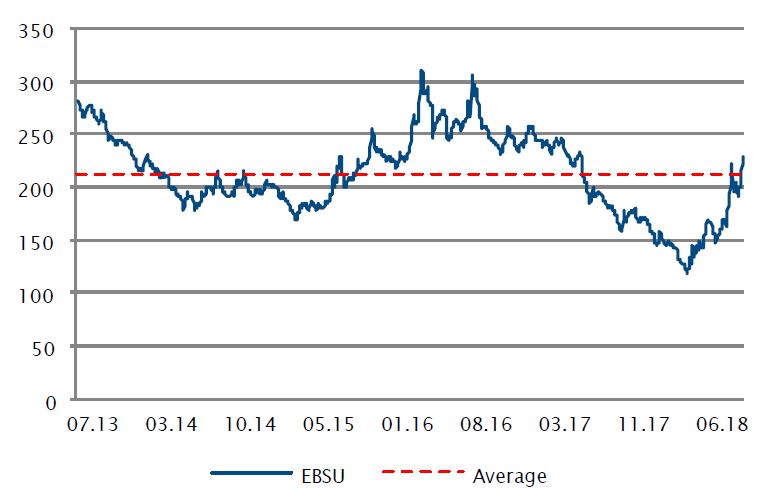

The bullishness in credit markets we saw at the end of 2017, which continued into the first weeks of January 2018, got abruptly disrupted by inflation fears, followed by trade concerns that were seen as a potential threat to global growth and finally political uncertainty in Italy. The result was a widening of spreads across credit sectors that did not leave banks unaffected. The banking sector of the European financial subordinated index (ICE BofA European financial subordinated index (EBSU) reported a spread widening of approximately 65 basis points from 140bps at the start of January to 207bps at the 25th of July.

Focus

European Banks and the search for value

Friday, 08/03/2018European banks remain one of our highest conviction sectors within credit as a number of developments in monetary policy, banking fundamentals and regulatory changes should support positive performance during the rest of the year.

Michalis Ditsas

Investment Specialist

A combination of solid fundamentals and positive valuations indicate that European banks are an attractive opportunity within credit.

EBSU option adjusted spread and average

Source

Sources: Bloomberg, SYZ Asset Management. Data as at: 30 June 2018

Interestingly, the European AT1 (Additional Tier 1 securities) market spread widening was entirely price/market sentiment driven, as there were no significant rate movements, indicating that this widening could be materially reversed to the extent that peripheral political risks recede. Monetary policy conditions, bank fundamentals and new financial regulations support the above view. Consider the following:

Monetary Policy

As discussed in our European credit outlook for H2 2018, today there is a very low risk of unexpected ‘hawkish’ shocks as the hiking cycle signalled by the Fed is already priced in and the ECB has continued to be transparent in reaffirming its very cautious and supportive stance. The market is discounting an increase in risk free rates but this will have limited impact on risky asset valuations. Furthermore, the establishment of emergency monetary policy mechanisms, namely the ESM, OMT and banking union, are reinforcing the toolkit that the ECB has at its disposal in order to ensure price and financial stability across Europe.

Bank Fundamentals

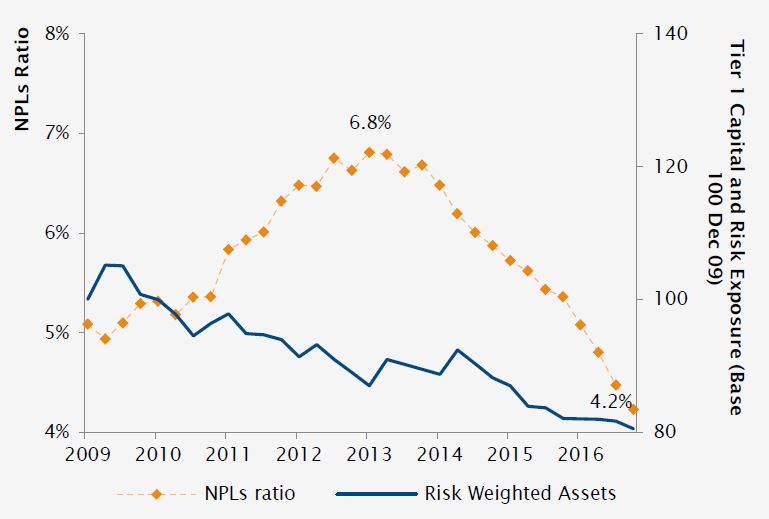

The financial system continued its balance sheet strengthening with higher levels of equity capital and improved asset quality. Eurozone banking institutions have piled on billions of fresh equity capital since the end of 2010, at the same time reducing their bad loan exposure from 2015 peaks to the current Non-performing Loan ratio of 4.9%.

Financial Regulations

The ECB recently announced further steps towards addressing the stock of banks NPL’s by shifting from a common target for the entire EU banking system to a supervisory approach that will consist of bank-specific targeting of NPLs reductions in order to avoid discrepancies between banks and among countries. In addition, the ECB can impose Pillar 2 requirements that would force banks to address any NPL issues. This increase in financial regulations is a positive development for Italian and Spanish banks in particular as it will reduce the risk of sudden recapitalization and the forced sale of NPL’s. For investors, a practical impact of these regulations will be the likely increase in issuance which will provide further investment opportunities.

Core Equity more than doubled over the last 10 years

Source

Sources: EBA Risk Dashboard, Bloomberg, SYZ Asset Management. Data as at: 29 December 2017

Derisking & asset quality improvement

Source

Sources: EBA Risk Dashboard, Bloomberg, SYZ Asset Management. Data as at: 29 December 2017

Favourable tailwinds, but a robust approach needed

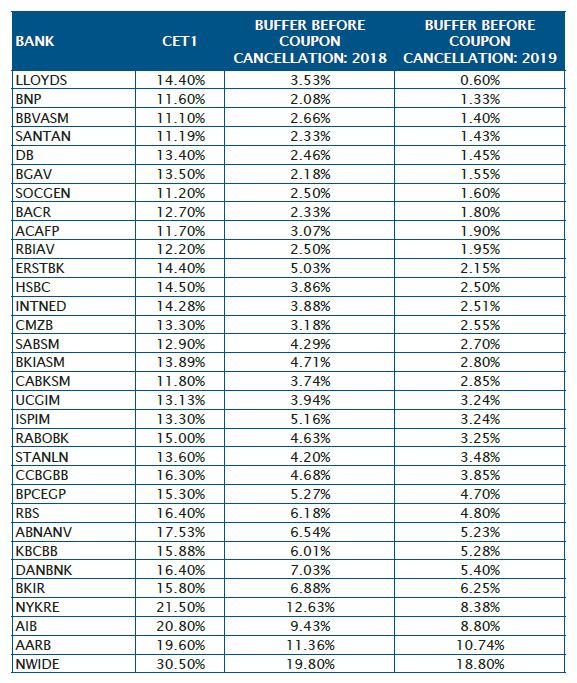

Our credit team uses proprietary models to evaluate the robustness of banks by stress testing balance sheets and estimating the probability of adverse events (e.g. conversions/coupon cancellations) for instruments such as CoCos (Contingent Convertibles). The results indicate that all 32 banks in our sample have sufficient buffer not only for 2018, but also for the more demanding regulations that they will face during 2019. (Fully loaded CET1 ratio updated at Q1 2018, while capital requirements could be revised by regulators after the outcome of the stress tests and the SREP process)

Conclusion

Spreads of the ICE BofAML Subordinated Euro Financial Index have rebased around the 5 year average, which results in attractive valuations. In addition, CoCo’s are offering attractive carry relative to other asset classes. These characteristics combined with solid banking fundamentals, positive regulatory developments, political risks that are either priced-in or have faded out and an overall stable economic environment make the asset class one of the most attractive places to invest this year.

Our proprietary models indicate that banks can withstand the impact of increased regulation

Source

Sources: SYZ Asset Management. Data as at: 31 July 2018

Disclaimer

This marketing document has been issued by Bank Syz Ltd. It is not intended for distribution to, publication, provision or use by individuals or legal entities that are citizens of or reside in a state, country or jurisdiction in which applicable laws and regulations prohibit its distribution, publication, provision or use. It is not directed to any person or entity to whom it would be illegal to send such marketing material. This document is intended for informational purposes only and should not be construed as an offer, solicitation or recommendation for the subscription, purchase, sale or safekeeping of any security or financial instrument or for the engagement in any other transaction, as the provision of any investment advice or service, or as a contractual document. Nothing in this document constitutes an investment, legal, tax or accounting advice or a representation that any investment or strategy is suitable or appropriate for an investor's particular and individual circumstances, nor does it constitute a personalized investment advice for any investor. This document reflects the information, opinions and comments of Bank Syz Ltd. as of the date of its publication, which are subject to change without notice. The opinions and comments of the authors in this document reflect their current views and may not coincide with those of other Syz Group entities or third parties, which may have reached different conclusions. The market valuations, terms and calculations contained herein are estimates only. The information provided comes from sources deemed reliable, but Bank Syz Ltd. does not guarantee its completeness, accuracy, reliability and actuality. Past performance gives no indication of nor guarantees current or future results. Bank Syz Ltd. accepts no liability for any loss arising from the use of this document. (6)