The hunt for yield will continue to be the main fixed income allocation driver in 2020. This makes sense; with 51% of the sovereign non-USD market, and one quarter of the fixed income asset class exhibiting negative yields, it comes as no surprise that investors will continue to seek opportunities in high yielding credit.

Last year was characterized by mounting geopolitical tensions, global economic slowdown, persistent manufacturing weakness, soft inflation and accommodative central banks. But not all was negative as the services sector remained resilient, supported by strong domestic demand and improving labour markets. In this environment credit markets generated fantastic returns with US high yield (USHY) returning 14.4%, European high yield (EHY) 11.3%, the European financial subordinated index (EBSU) 10.3% and the contingent convertible (CoCo) index 17.6%. These results exceeded our expectations at the start of 2019, where in the “Catch me if you can” analysis we pointed to total returns for the US and European HY above 10% and 7% respectively. What should investors expect from credit markets in 2020? Before we answer this question, let’s take a closer look at the credit market fundamentals, technicals and valuations:

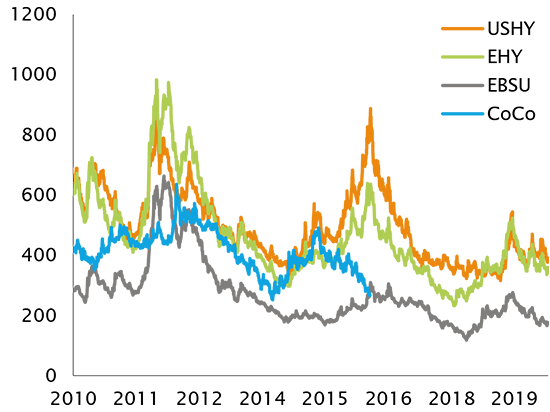

Spreads tightened across all high yield markets in 2019, as investor behavior was dominated by a risk-on sentiment. Spreads have not been as tight as they were in late 2017 and early 2018, but carefully evaluating investment opportunities is becoming increasingly important.

“Fundamentals and demand remain strong in credit markets. We predict that 2020 will be another positive total return year, in particular for European high yield and subordinated bonds.”

The par-weighted US high-yield default rate ended 2019 at 2.63%, up +168bps since the YTD-low 0.95% in March, and up +80bp y/y. Despite this increase the default rate remains low relative to the long-term average of 3.44%, based on defaults that go back to 1980. As we have seen in the past, energy and metals / mining companies accounted for almost half of the year’s defaults, as 25 of 53 defaults (47%) came from these sectors. In the meantime, recovery rates over the last twelve months were 26.2%.

In European HY, on a notional-weighted basis, the default rate ended 2019 at 1.8%, down from 2.1% in September of the same year. Recovery rates were also high at 31% over the past year and exceeded the historical average of 30%.

It is worth noting that European HY is less affected by the energy market since it accounts for only 2.5% of the overall market, while in the U.S., this sector currently makes up 12.5%, despite all the defaults it has experienced.

Leverage levels in the US high yield market have remained stable for three quarters at 4.1x and below the recent highs of 4.6x in the second quarter of 2016. In European high yield the leverage level has stabilized at 4.3x, after the increase that started in late 2017.

Interest coverage ratios held broadly stable in the U.S. at 4.5x. Likewise, in European high yield the weighted-average interest coverage ratio held around 6x, which is 0.5x below the cycle high seen in Q4 2017, but still one of the highest levels since the beginning of 2005.

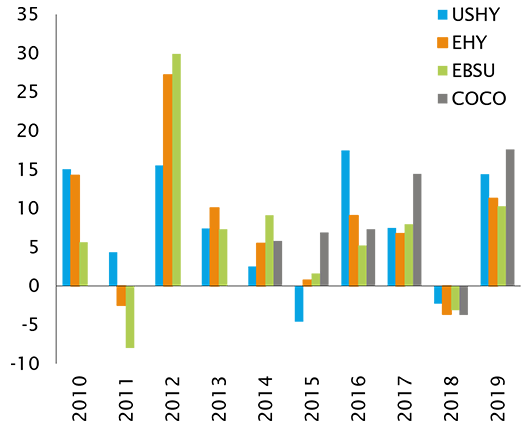

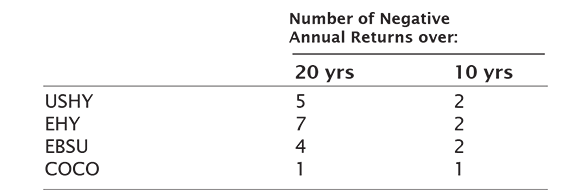

Below investment grade markets are very resilient and have produced positive total return performance through different market conditions. Over the past ten years, the US HY, European HY and the Euro Subordinated Financial Index (EBSU) performed negatively only twice, while the CoCo index only once (chart 2). Even when looking at the past 20 years, the period is dominated by positive returns (table A).

The above results should not come as a surprise since, as we discussed in “The Wonderful Benefits of High Yield in a Rising Rate Environment”, below investment grade bonds exhibit a low or negative long term correlation with traditional fixed income and equity-like performance with lower volatility.

Demand for below investment grade bonds remains strong since in 2019 we saw $19.3bn of fund inflows for US HY and €8.3bn for European HY, reflecting the favorable market conditions and investor sentiment. Issuance is expected to increase this year, but this will provide investment opportunities to investors and increase overall liquidity.

In the US, with the Fed expected to stay on hold for 2020, oil prices off the lows, but also higher defaults, low EBITDA and high debt levels, we would expect the market to return a mid-single digit in 2020.

Our preference, though, remains for EHY, particularly the Subordinated bond market. Central bank accommodation will remain in Europe over 2020, which will help corporations maintain their strong fundamentals and investor demand, and therefore coupon-like returns of 4% and 6.5% or above for the EHY and CoCo market are feasible.

That said, we steadily prefer EHY, as the European Central Bank’s strongly accommodative policy will not only help corporations maintain their strong fundamentals, but more importantly will support investor demand for risky assets and carry rich instruments. Among high yielding bonds, we continue to favor junior subordinated bonds such as CoCos and hybrids, due to their attractive yield and solid issuer profiles. As such, we believe coupon-like returns of 4% to 5% or above are feasible for the EHY and CoCo market over 2020.

Disclaimer

This marketing document has been issued by Bank Syz Ltd. It is not intended for distribution to, publication, provision or use by individuals or legal entities that are citizens of or reside in a state, country or jurisdiction in which applicable laws and regulations prohibit its distribution, publication, provision or use. It is not directed to any person or entity to whom it would be illegal to send such marketing material. This document is intended for informational purposes only and should not be construed as an offer, solicitation or recommendation for the subscription, purchase, sale or safekeeping of any security or financial instrument or for the engagement in any other transaction, as the provision of any investment advice or service, or as a contractual document. Nothing in this document constitutes an investment, legal, tax or accounting advice or a representation that any investment or strategy is suitable or appropriate for an investor's particular and individual circumstances, nor does it constitute a personalized investment advice for any investor. This document reflects the information, opinions and comments of Bank Syz Ltd. as of the date of its publication, which are subject to change without notice. The opinions and comments of the authors in this document reflect their current views and may not coincide with those of other Syz Group entities or third parties, which may have reached different conclusions. The market valuations, terms and calculations contained herein are estimates only. The information provided comes from sources deemed reliable, but Bank Syz Ltd. does not guarantee its completeness, accuracy, reliability and actuality. Past performance gives no indication of nor guarantees current or future results. Bank Syz Ltd. accepts no liability for any loss arising from the use of this document. (6)