Indeed, several elements indicate that we are facing some structural inflation, i.e. not or only slightly affected by a potential drop in demand. Among the factors which could keep inflation high:

1. De-globalisation. In the wake of the pandemic, governments of developed countries have become aware of their vulnerability to the risks associated with globalisation and the offshoring of supply chains.Their wish to repatriate part of the production back to their home country (or at least closer) was further accentuated by Russia's invasion of Ukraine. As a result, the coming decade could be characterised by a reshoring of production. This trend is inflationary;

2. The commodities supply shock. In the past, the price of a barrel of crude oil could not remain permanently high because it was facing self-destruction of demand. This scenario seems less plausible today. On the demand side, most governments have already put in place some subsidies, which do not help the inflationary situation. On the supply side, the response of governments since the beginning of the Russo-Ukrainian conflict has been slow. Let’s also keep in mind that the crisis we are facing is not only about energy. Unlike during the 1970s oil crisis, this time it is a supply shock for almost all commodities as Russia is a major exporter not only of oil and gas but also of industrial and precious metals, agricultural commodities, etc. The sanctions against Russia came at a time when the world was already facing an imbalance between supply and demand for commodities. The addition of these factors created a crisis that we have never faced before;

3. Fiscal policy. Without the possibility of monetary stimulus, governments in the developed world have no choice but to resort to expansionary fiscal policies. Admittedly, they are more targeted than during the pandemic. But they continue to widen budgetdeficits, prompting central banks to maintain "financial repression". In other words, nominal rates are rising but real rates have never been so negative. The reason: positive real rates would weigh heavily on deficit financing and could lead to a sovereign debt crisis. The corollary of financial repression: it seems very difficult, if not impossible, to fight inflation with negative real rates. In the 1970s, Paul Volker used positive real rates of over 2% to beat inflation. It should be remembered that despite all the hawkish rhetoric from the Fed in recent months, the money supply in the US continues to grow by around 11% over a rolling 12-month period. This increase is certainly less significant than during the covid crisis, but it is difficult to reconcile the fiscal situation with a decline in inflation;

4. The ultra-domination of certain large companies. One of the big surprises of the first quarter of 2022 was the resilience of the margins of S&P 500 companies. Despite the rise in input costs, companies have managed to maintain their level of profitability by passing on the increase in prices to consumers. This could be explained by the fact consumers are doing well (unemployment at its lowest level in decades, comfortable savings rates, etc.). But another reason might be that some large companies (notably the famous FANGs) enjoy a quasi- monopolistic status that allows them to impose their prices. This is also a structurally inflationary factor;

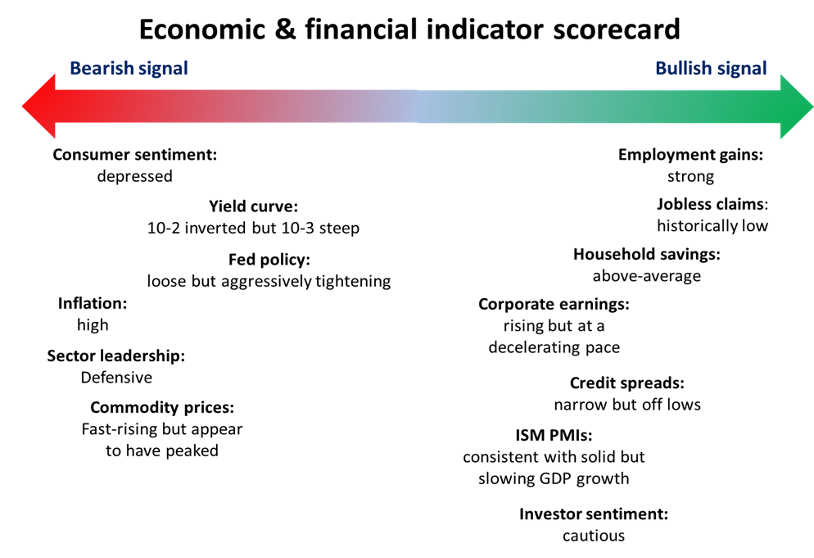

5. The power of habit. Financial markets have experienced several decades of deflation and disinflation. In the current context, the consensus believes that higher rates will lead to lower rates the following year. Flattening or even inverting the yield curve may actually be counterproductive for the Fed as financial conditions are not sufficiently restrictive to slow activity and therefore contain price increases. Consider the housing market, for instance. True, the rise in 30-year mortgage yields has been relatively brutal in recent months. But it is probably not enough to slow the sharp rise in house prices - and hence rents - in the US.

For the US Federal Reserve, slowing down an economy that is overheating and facing numerous capacity constraints in a context of de-globalisation, war and historically low unemployment (see below) is a very complex exercise. But does this necessarily mean we are entering a long and painful period of stagflation?