Another upside risk for commodities prices is the fact that the EU could declare a full embargo on Russian oil after this weekend's French election. It seems that pressure from Brussels on Russia is increasing as they understand that despite their clear intentions to cripple Russian energy production, loadings of Russian oil have so far been surprisingly resilient, so much so that Russia's current account balance is at all-time highs. The following are various scenarios potentially considered by the Europeans:

1. A full and immediate embargo: this is likely to hurt European consumers more than Russian producers in the near term. According to JP Morgan, a full, immediate ban would likely drive Brent crude oil prices to $185/ bbl as more than 4 mbd of Russian oil supplies would be displaced with neither room nor time to re-route them to China, India, or other potential substitute buyers;

2. Special taxes and;

3. Price caps on European imports of Russian oil.

The later two alternatives are plausible. Indeed, because the operational breakeven for Russian oil is less than $10/ bbl, Russian producers could likely still afford to continue to deliver oil to European consumers, even under tariffs of 90% or a price cap of $20/bbl. Either of these options may provide a politically-acceptable middle ground, allowing the EU to make a show of force while maintaining its Russian energy lifeline. The first option will put additional upward pressure on oil prices and the broader commodity spectrum.

A specific area of stress within commodities is Food. Indeed, the Food and Agriculture Organization announced a few days ago that its FAO Food Price Index, which tracks monthly changes in the international prices of a "basket of commonly-traded food commodities" was up 12.6% in March vs. February (m/m). It's also 33.6% higher than it was last March (y/y).

The FAO says the war "spread shocks through markets for staple grains and vegetable oils." Russia and Ukraine collectively accounted for about 30% of global wheat exports and 20% of maize exports over the last three years, the organization said, with conflict-related export disruptions in both countries prompting a surge in global prices of wheat and coarse grain. The FAO Cereal Price Index was 17.1% higher in March than it was in February.

Another example of soaring soft commodities prices is corn. The global outlook for corn supplies has plunged since Russia's invasion of Ukraine began in late February. Ukraine supplies a fifth of the world's corn and could experience a 50% decline in output this year.

Soaring fertilizer costs have forced some farmers in the U.S. to increase plantings of soybeans this growing season versus corn as the crop requires fewer nutrients. Fertilizer prices are at record highs because of rising natural gas costs and Russia limiting fertilizer exports to 'unfriendly' countries. Russia is one of the biggest exporters globally -- the U.S. is a large importer of nitrogen and potash from Russia.

And the latest development pushing corn prices through the roof is the Biden administration's announcement of emergency measures last week to expand biofuel sales to curb soaring gasoline prices. The problem with this move is that the ethanol industry absorbs a larger share of the corn crop, which would curb supplies to the food industry. So ultimately, it would increase prices.

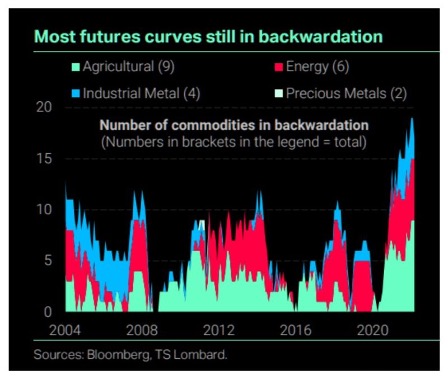

These examples show how commodities are interconnected. The rise of energy prices has some ripple effects on other commodities and means that the world is not just facing an oil supply shock as in the 70s but a broad commodity supply shock.

Global food prices have risen to levels even higher than those that led to the inflation riots of 2010/11, known as Arab Spring. Indeed, soaring food prices are creating new geopolitical risk such as social unrest not only in emerging markets but also developed markets, the rise of populism, massive immigration, etc. These risks need to be embedded into markets risk premium as well.