.png)

On 14 February, Justin Trudeau's government decided to impose financial sanctions on some of the activists of the Freedom Convoy, a grassroots movement that blocked Ottawa in protest against the compulsory Covid-19 vaccination. A few days later, the Canadian police announced that more than 200 bank accounts linked to the protest movement had been frozen. This was an unprecedented event in a developed country with a clear message: if the government doesn't like how you use your money, it can decide overnight that you no longer have control over it.

Two weeks later, a confiscatory decision of a completely different dimension was made: in retaliation to the invasion of Ukraine, the West decided to freeze the assets of the Russian Central Bank. The US, Canada, France, Italy, Germany and the UK want to "prevent the Russian Central Bank from deploying its international reserves in a way that undermines the impact of sanctions". About half of the $630 billion in reserves that could have been used by the Russian Federation to defend the ruble (in free fall) and to recapitalise local banks (cut off from SWIFT) are unavailable to Moscow today.

The international monetary system

This extraordinary decision is likely to call into question the international monetary system that has been in place for more than 50 years now. As financial research provider Gavekal recently reminded us, the financial order as we know it is based on the following:

- Energy prices and the vast majority of world trade are denominated in US dollars;

- The US faces a structural current account deficit, which allows the rest of the world to have access to the dollars needed for international trade;

- Countries with a current account surplus put their surplus dollars into US Treasury bills as a reserve (a boon to the US budget which is also in structural deficit and therefore needs to be continuously refunded);

- If necessary, the US Federal Reserve stands ready to inject dollars into the global system via foreign exchange swaps or directly into the US economy (which de facto benefits the global economy).

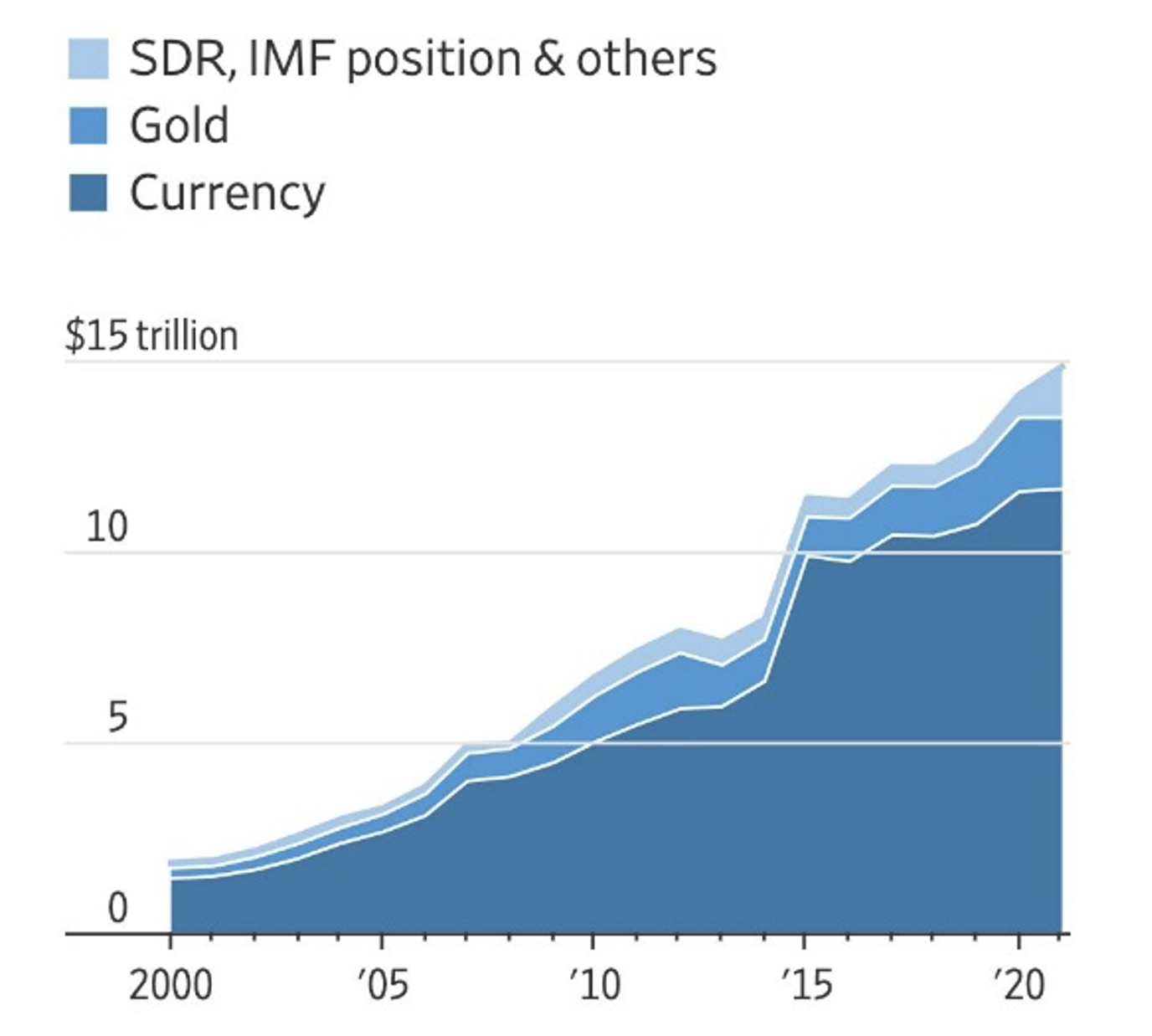

The hoarding of international currency reserves is a cornerstone of the current monetary system. Indeed, global currency reserves have exploded over the last twenty years, from $1.8 trillion in the early 2000s to $12.8 trillion at the end of last year. These reserves are mainly held in US and European government bonds and bills, with the US dollar still accounting for almost 60% of these reserves and the euro for about 20%. As the chart below shows, total reserves amount to almost $15 trillion, as central banks also hold other assets such as gold - more on this later.

Although this system has created many excesses and disparities, it has worked quite well since the end of Bretton Woods, and in particular for the Americans who have found a way to finance their twin deficits.

Official reserves held by central banks

Source: IMF

On the monetary policy front, the Fed is likely to hike rates but probably less than what the current Fed dots imply. The ECB is unlikely to hike rates despite energy prices keeping inflation much higher than the ECB target.

Towards a new paradigm?

But for many observers, the fact that the West has chosen to freeze dollar (and euro) reserves will prompt some central bank governors to rethink the logic of reserve accumulation and also the wisdom of investing part of the balance sheet in US Treasury bonds. With negative real yields (-5% for the 10-year), US bonds have no other reason to exist than the security they offer to their holders. But if Washington can decide overnight to freeze the dollars that a sovereign country thought were its own, won't the governors of the central banks of China, Pakistan, India, Turkey, Kazakhstan or Saudi Arabia be prompted to sell all or part of their dollars and diversify their holdings into other assets? Of course, the circumstances surrounding this unprecedented decision by Western countries are quite exceptional and are not expected to be repeated (at least we hope so...). However, the freezing of the Russian central bank's assets could have the following consequences.

1. Foreign currency reserves will lose some of their usefulness

There are two reasons for holding reserves: to intervene or stabilise domestic markets, or to act as a war chest in the event of an economic shock, natural disaster or balance of payments crisis. For Professor Barry Eichengreen of UC Berkeley, an expert on global reserve management, it is the use of reserves as war chest that could be challenged, with the effect of reducing the demand for said reserves. An important consequence is that if sovereign states see reserves as less useful and/or less available, then they will have to accept the inevitability of a higher volatility in their exchange rates.

2. The urgency of reforms in emerging countries

Professor Eichengreen argues that the diminishing role of reserves will push governments to strengthen their financial systems and make their economies less sensitive to exchange rate volatility, for example by discouraging companies from borrowing in foreign currencies. This in itself could have a profound impact on global markets and on the model of emerging markets and developing economies.

This view is partly shared by Jim O'Neill, an economist at Goldman Sachs. He believes that this paradigm shift will push emerging countries to implement more reforms, open up their domestic markets, liberalise their economies and in a way break away from their dependence on the US monetary hegemony.

3. The dollar's loss of momentum as a reserve currency

This is a hypothesis put forward by Zoltan Poszar, a money market specialist at Credit Suisse and former employee of the New York Federal Reserve. Historically, wars have often been a turning point for the monetary system. Russia's invasion of Ukraine and the sanctions that followed could indeed act as an electroshock. For Poszar, the accumulation of dollar reserves by central banks makes less and less sense. The freezing of Russian assets will push many central banks to diversify away from the dollar and re-anchor their local currencies to assets that are less likely to be influenced (or confiscated) by Western governments.

4. A new monetary order

According to Poszar, a new monetary order could emerge in which states are much less interconnected via international bank accounts and reserves.

So far, most reserves have consisted of debts owed by one state to another. This is the case, for example, for a central bank that holds US treasury bills or dollars deposited with JP Morgan. It is this type of asset that can indeed be seized or sanctioned.

In the future, many states may be tempted to hold assets that they can control at all times - for example, gold held in a vault at a domestic bank.

The temptation is therefore great for Russia, China and other emerging countries to peg their currencies to the gold standard, which would be somewhat of a return to Bretton-Woods. A U-turn that would reduce the ability of the West to use the dollar or the euro economic warfare.

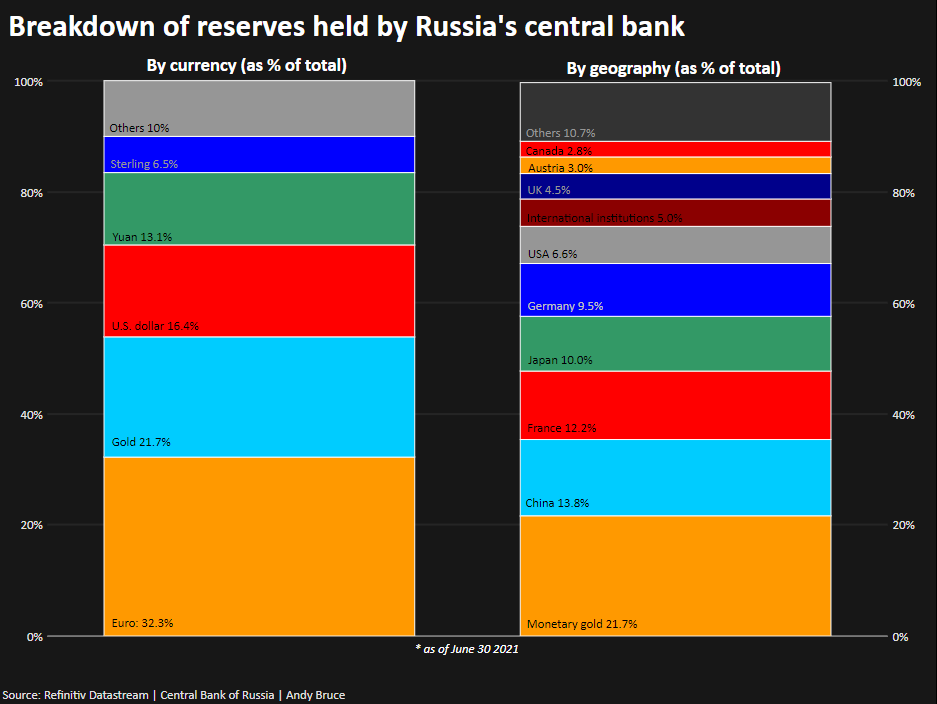

It should also be noted that this de-dollarisation movement was initiated by Russia several years ago already. Since the annexation of Crimea in 2014, Russia has gradually divested itself of its US Treasury bonds and reinvested its assets in euros, yuan, sterling and also gold. In fact, today the Russian central bank holds more gold than US dollars.

Which asset(s) to replace the dollar?

While many countries are probably tempted to reduce their dependence on the dollar and the euro, they face a major problem: how and in which asset to reinvest the trillions of dollars currently held as reserves?

Until the Ukrainian crisis, the euro was the main alternative to the dollar. But the alignment of the Europeans with the Americans in this conflict is not likely to strengthen the appeal of the euro for states that want to free themselves from this type of risk.

The yuan is also one of the alternatives, especially as China is becoming increasingly important in trade.

Gold is of course a natural candidate. Central banks have accumulated an additional 463 tonnes of gold in 2021, bringing global gold reserves to around 35,600 tonnes, their highest level in almost 30 years...

But gold as a reserve asset has its limits. Firstly, its market value, which is currently around $12 trillion, is low compared to the $29 trillion or so in annual trade.

Another limitation of gold is that it is not so easy to store and transfer.

These limitations are all factors that could lead some central banks to consider crypto-currencies such as bitcoin as a possible reserve currency: limited supply, decentralisation, ease of storage and transferability are all factors that make bitcoin a candidate as a reserve asset for central banks. However, this asset also has its risks and limitations: even lower market value than gold, legal risk, high volatility, etc.

Even if the movement towards reserve diversification is underway, de-dollarisation cannot happen overnight. But it is likely that the composition of central bank balance sheets will be scrutinised even more closely by economists and governments alike, as the macroeconomic and financial consequences of asset reallocation by central banks could be considerable.