Active share is a measure of the percentage of a portfolio's holdings that differs from its benchmark.

A manager is considered truly active (i.e. making significant bets against the index) when the active share is above 60%. Historical performance data indicates that fund managers with a high active share tend to outperform their benchmarks.

What is the link between high active share and above-average relative performance?

According to some studies, funds with a high active share (and therefore with a high degree of concentration) share the following characteristics

• Long-term investment prospects: the concept of market "myopia" has shown that markets are much more difficult to predict in the short term than in the long term. Managers who have a propensity to invest over time tend to outperform;

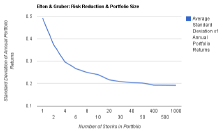

• Better access to information: managers who hold fewer stocks in their portfolios can allocate more time and resources to analysing these companies and develop a better understanding of the stocks they invest in, avoiding panic in downturns

• Greater conviction on their active bets: an informational advantage, such as a deep fundamental understanding of a company or sector, gives active managers the confidence to focus their portfolios in areas of the market where they have deeper knowledge. In addition, the decision to build a concentrated portfolio usually comes when the portfolio manager feels he/she knows enough about his/her holdings to more than offset any potential risk.

If conviction-based portfolio management leads to better relative performance, why don't most managers adopt this approach?

There are several explanations for this:

1. Career risk: as JM Keynes said, "it is always more comfortable to fail conventionally than to succeed unconventionally". In the fund management business, a marked underperformance for two years in a row can lead to the manager's ouster. In order not to jeopardise their careers, most managers prefer to stay close to their benchmarks and invest in stocks and sectors that enjoy a consensus;

2. Biased remuneration formulas: for the most part,the fund management business model is based on fees calculated as a percentage of assets under management. This formula encourages managers to focus on the growth of fund assets rather than performance. Indeed, since unit holders do not tend to pay back the fund in case of poor performance, managers are not inclined to take too much risk. On the other hand, few managers consider closing the fund to new clients when the fund size becomes too large. To avoid these capacity problems, most managers prefer to invest in large benchmark weights, whose potential for appreciation is often less attractive than some "outside the box" ideas;

3. The regulatory aspect: In the US, the Prudent Man Rule pushes fund managers to avoid risk through diversification. In Europe, fund managers are guided by specific regulations designed to prevent fund assets from becoming too concentrated (e.g. the 5/10/40 rule within UCITs).