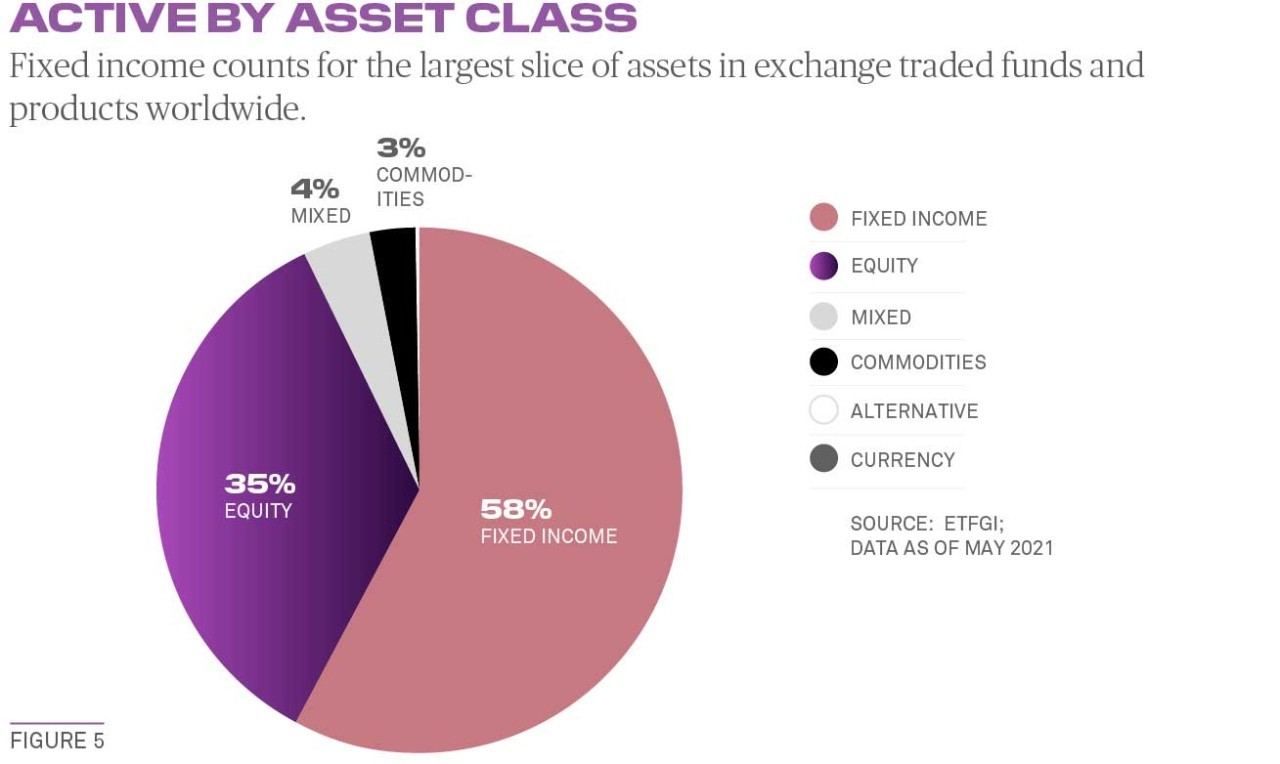

ETFs (Exchange Traded Funds) are becoming increasingly popular. They combine the advantages of a mutual fund (diversification) with those of stocks (they can be traded on the stock exchange at any time) while offering a much lower TER (total expense ratio) than funds. Since their inception in 1993, the vast majority of ETFs have followed a so-called passive investment strategy. In other words, ETFs seek to replicate the performance of an equity, bond or commodity index without seeking to outperform. But in recent years, a new type of ETF has become increasingly popular. These are actively managed ETFs. Their objective is not to replicate the performance of an index, but rather to outperform it.

Charles-Henry Monchau

Chief Investment officer

The rise of ETFs

A new SEC rule as a game changer

The financial industry has long refrained from launching this type of product for regulatory reasons. Indeed, an ETF manager should be fully transparent about the complete portfolio breakdown, whereas a traditional investment fund manager can only publish the most important positions once a month. As a result, many active managers were shying away from launching ETFs because this transparency requirement exposed them to the risk of "front-running," a practice that involves having knowledge of the upcoming purchase of a fund and getting ahead of that trade. But in 2019, the SEC introduced a new U.S.-specific rule allowing ETFs to become "semi-transparent," i.e., publish their portfolios less frequently and "mask" individual positions by replacing them with a "proxy."

Since this regulatory change, actively managed ETFs have experienced strong growth. By the end of 2021, their assets under management amounted to $400 billion. Admittedly, this represents only a very small share (5%) of the approximately $9 trillion of ETFs available worldwide. But the momentum is undeniable. In 2021, 188 new ETFs were launched in the United States and two-thirds of them were based on active strategies.

Quelle

Bloomberg

The Ark Invest mania

The icon of active ETFs is Ark Invest. Cathie Wood, the company’s founder and CEO, was quick to recognize their growth potential. Easier to access and less expensive than investment funds, they combine the best of both worlds: active management and instant liquidity. This new type of ETF enables asset management firms to target a wider range of investors, particularly retail investors. To convince this often neophyte audience, Cathie Wood has surfed the wave of themes, including innovation and technology. Ark Invest Innovation raised more than 15 billion in assets last year, despite a very disappointing performance. Because Cathie Wood excels at marketing by using the required level of transparency as an advantage: she has made her research public, hosts podcasts and posts her beliefs on Twitter. So much so that emulators have started to emerge. Many investment fund managers have decided in the last year to offer some of their active strategies via ETFs. This is the case for DFA, Putnam, Fidelity and T-Rowe Price. Franklin Templeton and J.P. Morgan have announced their intention to do so this year. But if equities are well represented in the universe of actively managed ETFs, it is the bond strategies that take the lion's share. PIMCO launched the famous "MINT" ETF 10 years before the regulatory change. This ETF now has a market capitalization of 14 billion.

Quelle

Bloomberg

What’s next for actively managed ETFs?

Will the boom in active ETFs last? The crash of Ark-managed ETFs is likely to put off many investors. And for asset management companies, it is essential not to "cannibalize" their investment fund offerings because ETF management fees are much lower. The regulatory framework also imposes certain limits on the investment universe: the securities held must be tradable on stock exchanges at the same time as the ETF, which de facto eliminates foreign equities, OTC bonds or small caps with low liquidity. Management companies therefore have the possibility of sorting out and marketing actively managed ETFs only for certain strategies.

What about Europe? Surveys confirm the interest of institutional and retail investors for this new breed of ETF. But European regulations still require ETFs to disclose all their positions on a daily basis. A gap that will probably have to be filled one day.

Quelle

Bloomberg

Disclaimer

Dieses Werbedokument wurde von der Syz-Gruppe (hierin als «Syz» bezeichnet) erstellt. Es ist nicht zur Verteilung an oder Benutzung durch natürliche oder juristische Personen bestimmt, die Staatsbürger oder Einwohner eines Staats, Landes oder Territoriums sind, in dem die geltenden Gesetze und Bestimmungen dessen Verteilung, Veröffentlichung, Herausgabe oder Benutzung verbieten. Die Benutzer allein sind für die Prüfung verantwortlich, dass ihnen der Bezug der hierin enthaltenen Informationen gesetzlich gestattet ist. Dieses Material ist lediglich zu Informationszwecken bestimmt und darf nicht als ein Angebot oder eine Aufforderung zum Kauf oder Verkauf eines Finanzinstruments oder als ein Vertragsdokument aufgefasst werden. Die in diesem Dokument enthaltenen Angaben sind nicht dazu bestimmt, als Beratung zu Rechts-, Steuer- oder Buchhaltungsfragen zu dienen, und sie sind möglicherweise nicht für alle Anleger geeignet. Die in diesem Dokument enthaltenen Marktbewertungen, Bedingungen und Berechnungen sind lediglich Schätzungen und können ohne Ankündigung geändert werden. Die angegebenen Informationen werden als zuverlässig betrachtet, jedoch übernimmt die Syz-Gruppe keine Garantie für ihre Vollständigkeit oder Richtigkeit. Die Wertentwicklung der Vergangenheit ist keine Garantie für zukünftige Ergebnisse.