While the official statement was in line with market expectations, the press conference was much more hawkish than expected. European Central Bank (ECB) Governor Christine Lagarde is clearly showing signs of stress (or pressure from Germany? other Central Bank peers?) regarding European inflation. She said the risks are on the upside for the next few months - a “unanimous concern” among ECB members.

European inflation, which exceeded 5% in January, is likely to continue to be above the ECB’s 2% target for some time, driven mainly by commodities (the Russia-Ukraine conflict is not helping) and supply shocks, exacerbated by Omicron’s potential impact, however small, on China’s supply chains.

Christine Lagarde has set the stage for a significant shift in March. It could be seen as a pivot in ECB monetary policy. She also indicated that:

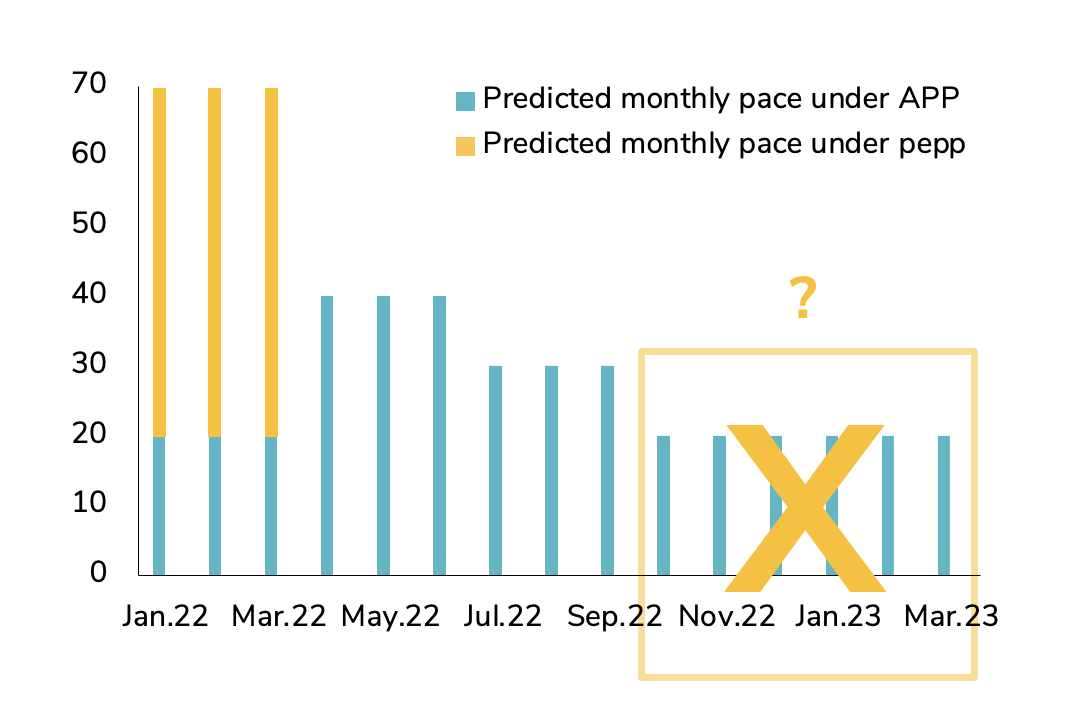

- PEPP (Pandemic Emerging Purchase Program) will end in March 2022;

- APP (Asset Purchase Program) will partially offset the end of PEPP through 40 billion euros a month in 2Q22, 30 billion euros a month in 3Q22 and 20 billion euros a month thereafter;

- It is not prudent to exclude a 2022 rate hike (10basis points?);

- The end of APP net buying in 3Q22 is possible.