Volatility made a comeback in the last few weeks, triggered by concerns that the US Federal Reserve could taper its monthly asset purchases at a faster rate and fears that the emergence of Omicron could weigh on global economic growth and contribute to supply chain disruptions.

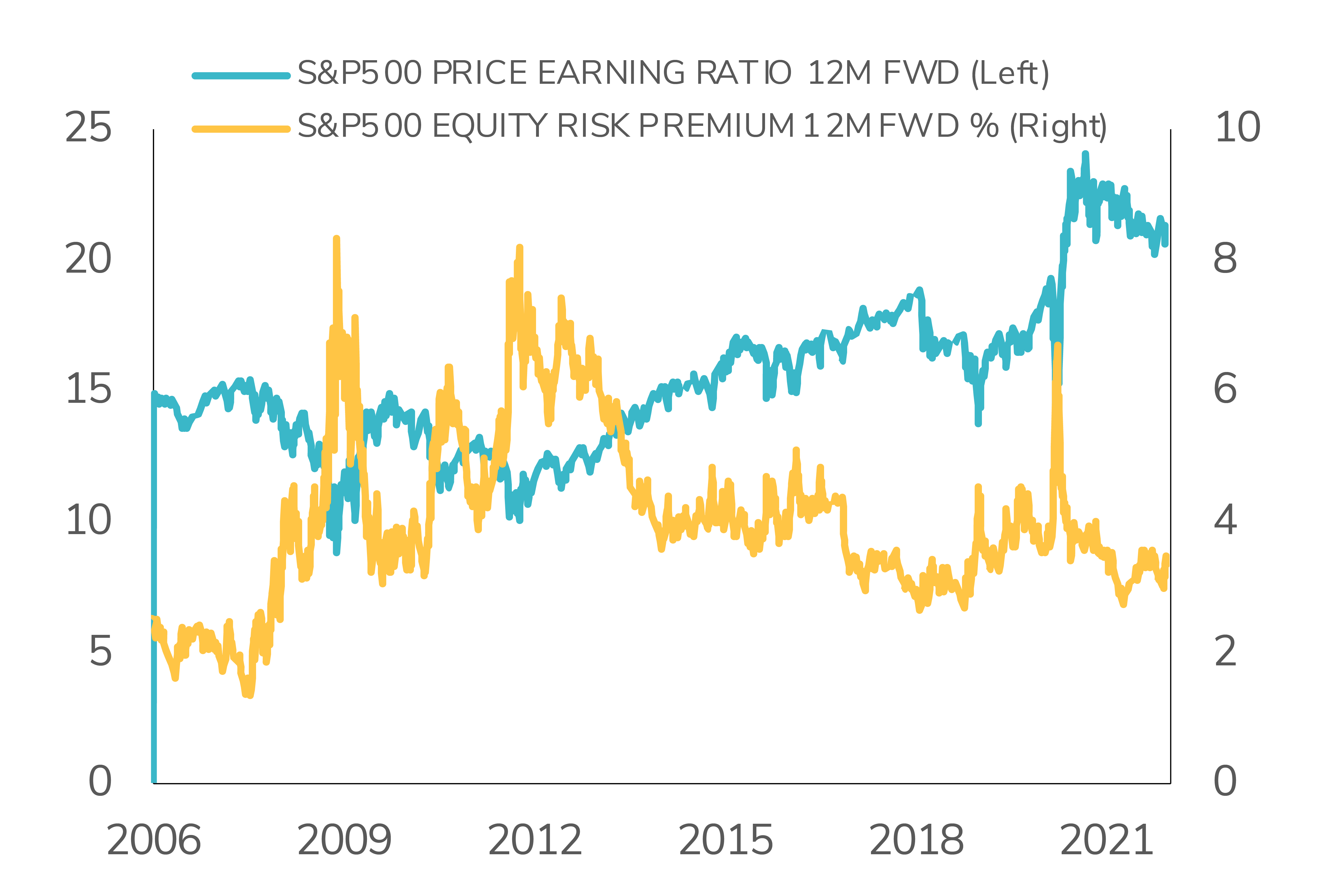

As we are heading towards a new year, we are concerned by the high level of valuations of some market segments (e.g. US equities) at the time of normalization of monetary policies. Moreover, some technical signals such as market breadth are pointing towards some negative divergence.

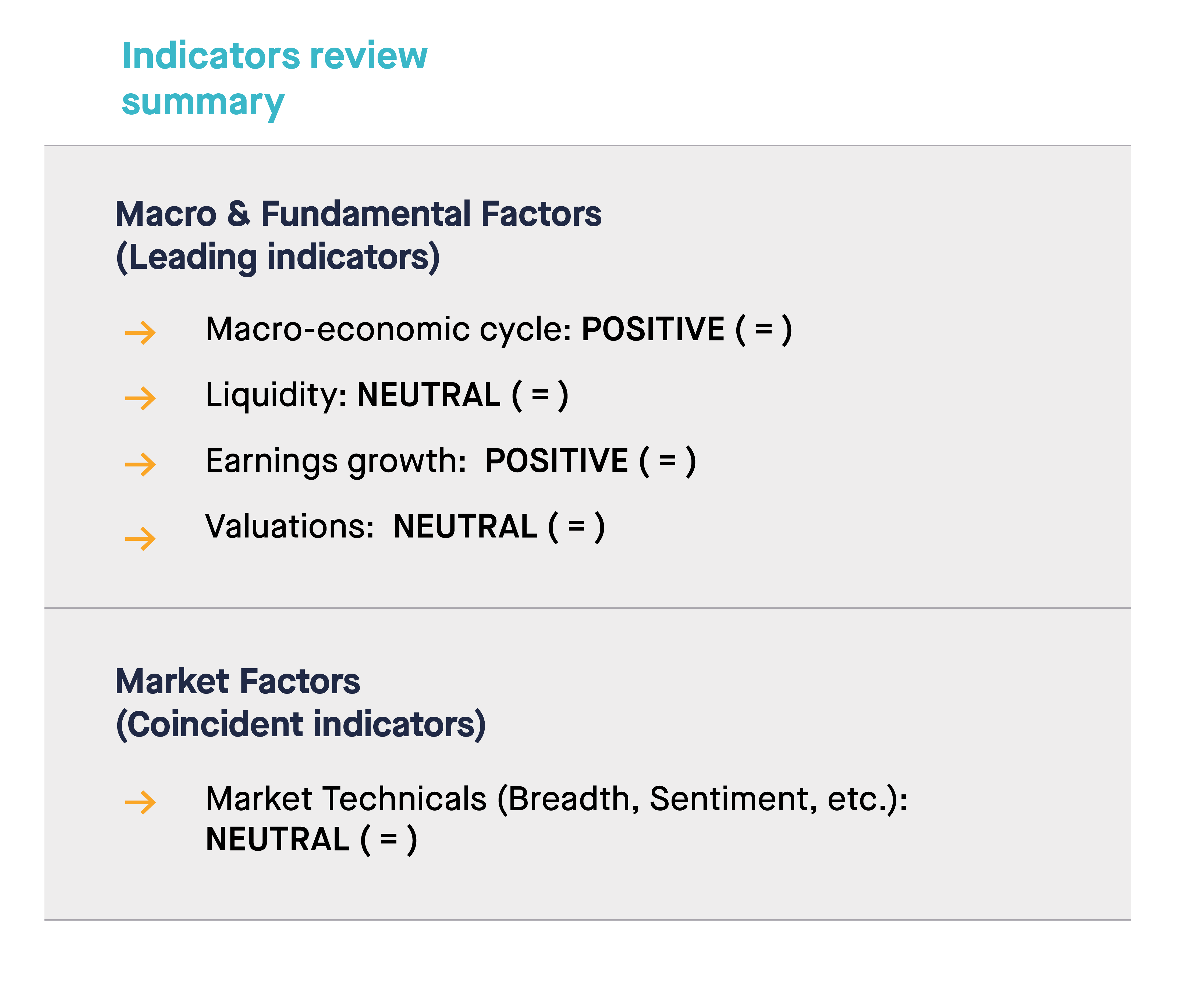

That said, the weight of the evidence leads us to keep a positive stance on risk assets and equity in particular. Here’s why:

- While we had obviously not predicted the irruption of this new variant, we had stubbornly high inflation as one of our three bear risks for 2022. For the time being and even with this Omicron variant, we remain within the scope of our macro-economic outlook, i.e. we believe that the worst of concerns about stagflation have mostly been priced into markets. We expect slower, though above potential, global economic growth in 2022 and inflation to gradually normalize, although it might stay sticky for a while;

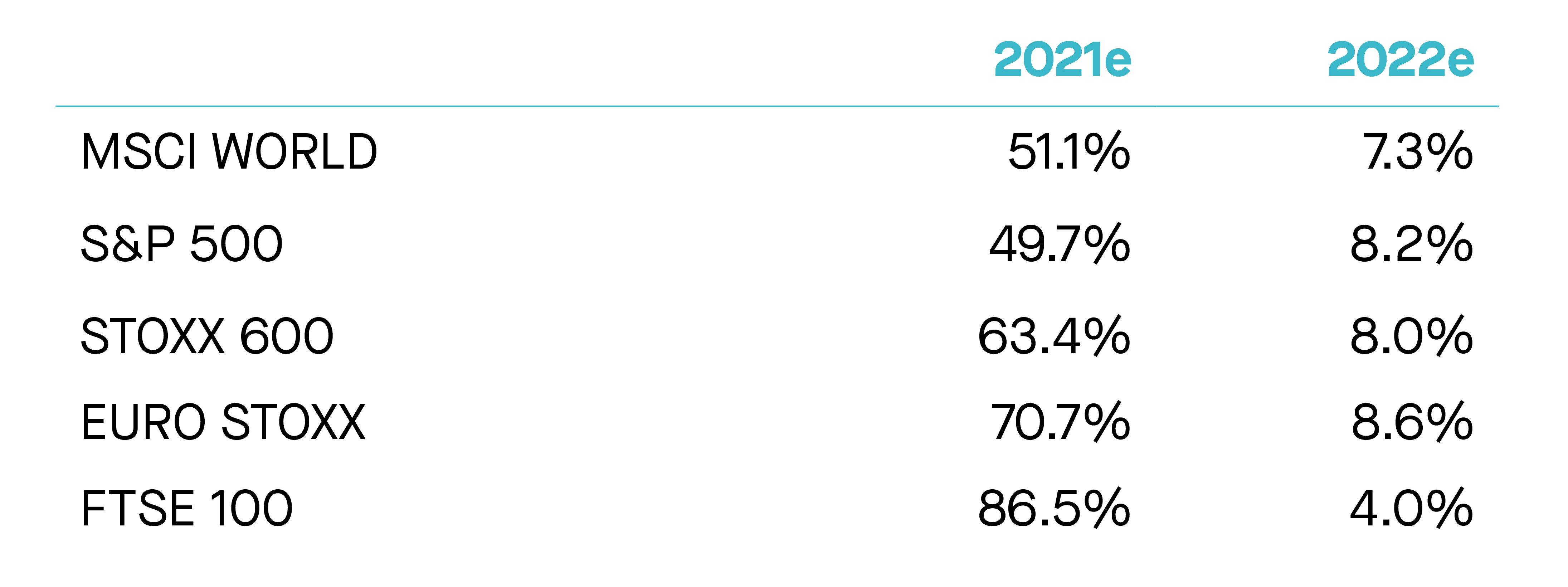

- In the near-term, we continue to believe that strong earnings growth will more than offset the coming gradual normalization in fiscal and monetary policy.

- Negative real bond yields in the vast majority of developed markets also incline us to favor risk assets over government bonds. However, we are adding some protections to the portfolios;

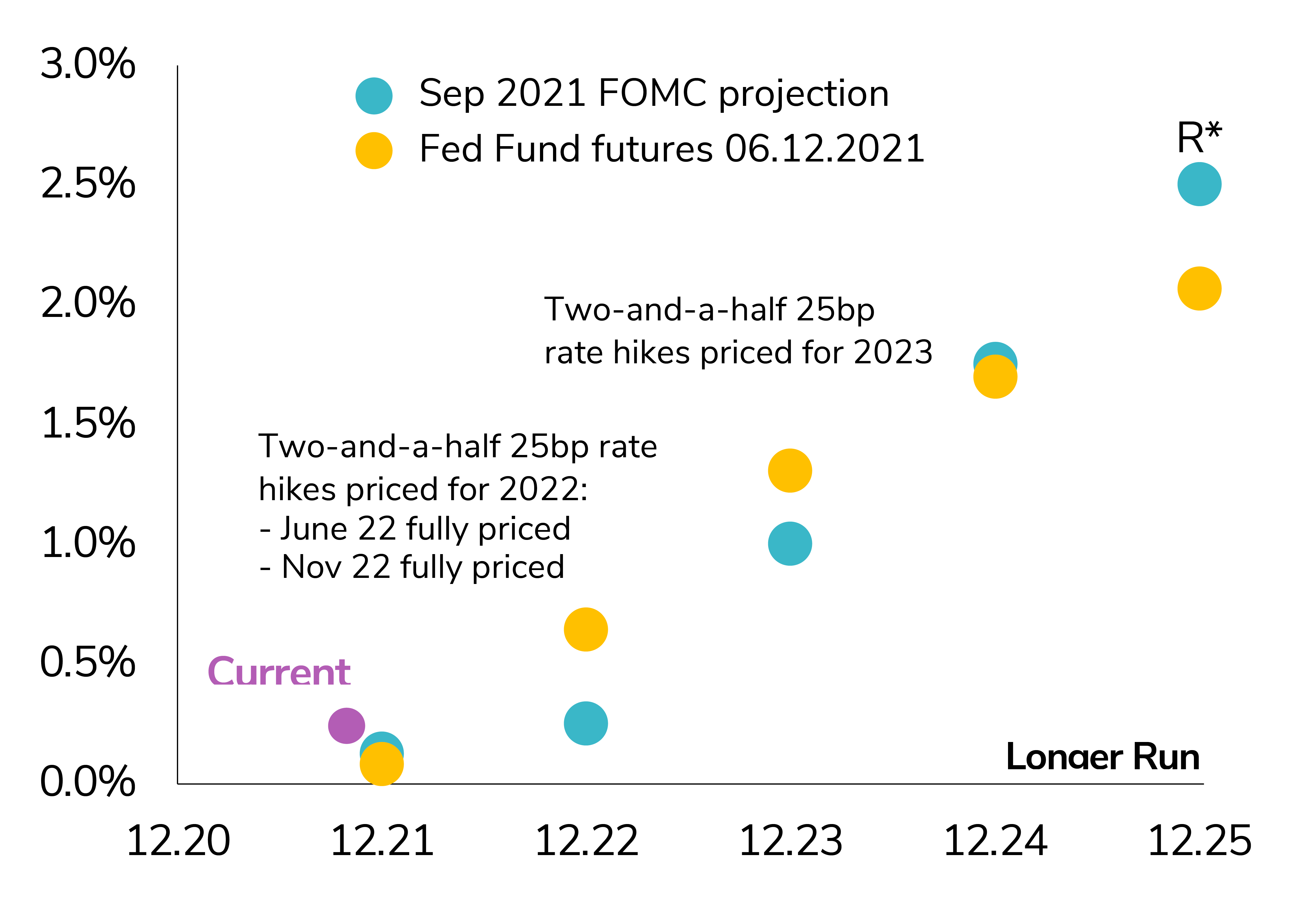

- From a tactical standpoint, we are downgrading rates, US government bonds and US Curve from cautious to disinclination due to upward risks on US long term rates. We still favor EUR Core curve over USD Curve;

- Within equities, we have a preference for Eurozone and Japan equities and are positive for US, UK and Swiss equities. We are cautious on China and Emerging Markets ex-China equities;

- We remain cautious on commodities and (short-term) bullish dollar.

- From a portfolio construction standpoint, we note that bond/ equity correlations are unstable at this stage which makes it difficult to diversify portfolios. Our tactical asset allocation is summarized in the matrix at the end of the article.