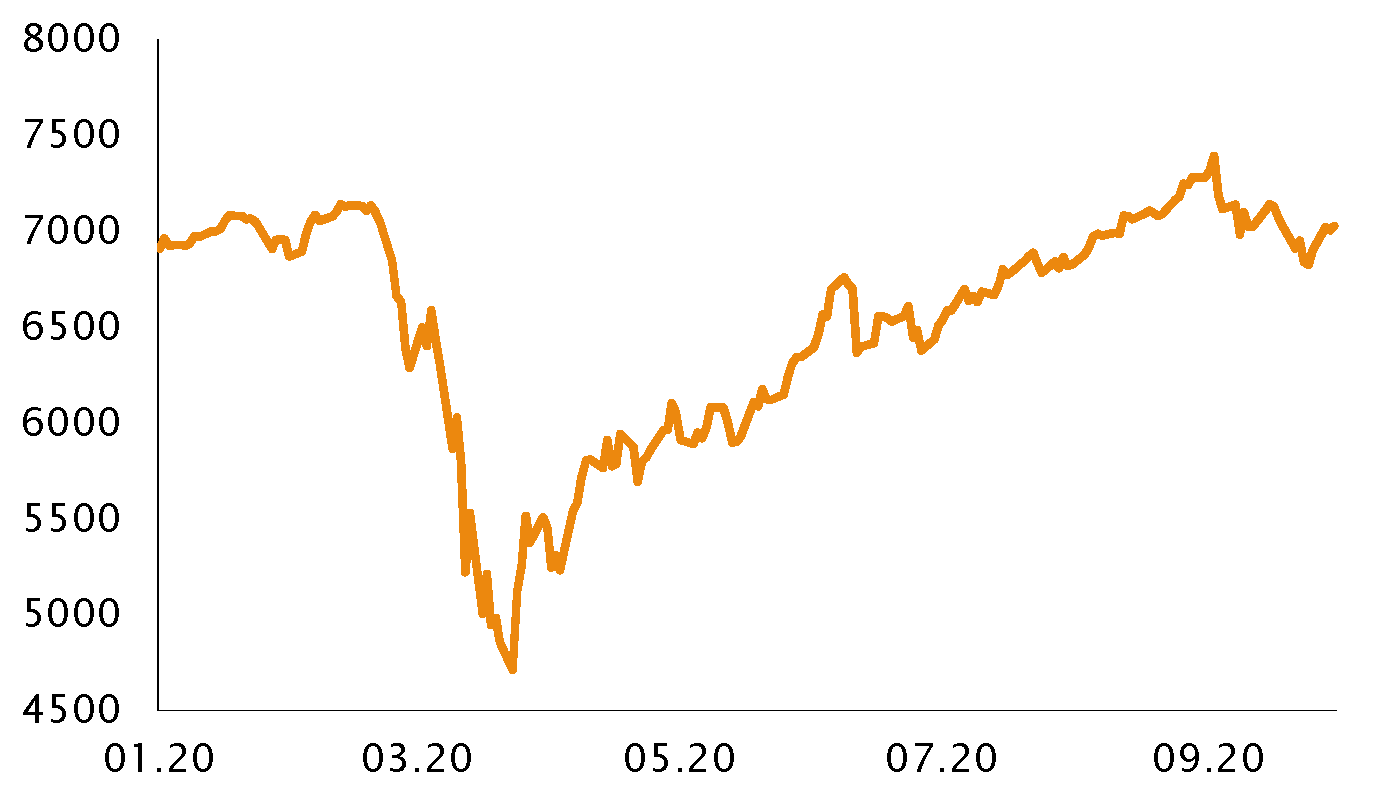

Between May and September 2020, the macroeconomic landscape recovered a bit but remains highly dependent on a vaccine and its efficiency. We have witnessed the end of an era where treasuries act as portfolio diversifiers and equities rallied to all-time highs, with of a bump in June fueled by fear of a second wave and characterized by an important sector rotation from momentum/growth to value. Strong equity returns were dominated by technology names and continued central banks support. Retail investors fearing to miss out the equity rally purchased calls massively towards the end of August, which was broadly seen as a market top for many investors and caused a tech sell-off.

Since our last letter in May and as expected, we have been in an exceptional trading environment for hedge funds. Most strategies have recovered their losses and some managers such as large multi-PM platforms and convertible arbitrageurs even post double digit performances for the year. The latter was one of our favorite theme for the last few years benefitting from a high level of new issuance and volatility. Some long/short equity with focus on growth sectors have also had stellar returns. There are some exceptions which have continued to underperform like quantitative strategies. Most surprisingly this is also the case for few blue chip managers and this is difficult to justify.

Explanations could be that the crowdedness in the medium frequency program (few days to months) or that models are not used to have this consistent high level of volatility. Hopefully, this level of volatility without large shock is favorable for most of the other strategies and we expect that heightened volatility will remain. We are therefore convinced that hedge funds are perfect instruments to benefit from the current environment.

At the end of this letter, we discuss a new strategy to generate alpha and diversification in the next years.

LIQUID ALTERNATIVES INVESTMENT INSIGHTS (MAY TO SEPTEMBER 2020)

Montag, 10/26/2020HIGHLIGHTS

- Macroeconomics recovered but depend on the outcome of a vaccine against COVID-19

- We believe the environment is optimal for hedge funds to keep making money

- Equity hedge managers rebounded nicely

- Quantitative strategies struggled amid crowdedness and persistent volatility

- Merger and acquisitions spreads continued to tighten

- Convertible arbitrageurs posted very good returns, helped by tightening credit spreads and record new issuances.

STRONG REBOUND FOR HEDGE FUNDS

EQUITY HEDGE

Equity hedge managers rebounded nicely after posting losses across the board in the first four months of 2020. Just like in the drawdown period, smaller managers outperformed. A lot of managers entered the recovery period with lower net and gross exposures in an effort to preserve capital in March.

As the year unfolded thereafter, they were able to redeploy capital and accordingly profited from the equity market rally. Managers generally benefited from a dislocated market with discrepancies. Specialists were able to pick COVID winners and avoid losers.

Earlier in the period under review, those managers who maintained exposures through the downturn performed best.

Net exposures remain at historical lows. Best performers had a tilt in tech and momentum, though value had a rally end of May. Extreme factors volatility and a growth to value rotation in June was challenging for many, before rebounding. August was illustrated by being the first month since April where hedge funds were not net buyers of equities, selling mainly Chinese equities. In the September sell-off, equity managers outperformed markets as they protected on the downside.

EVENT DRIVEN

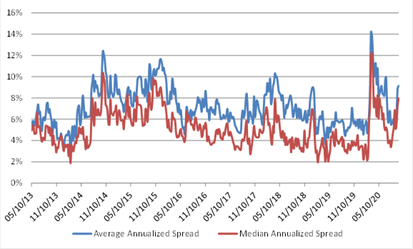

In March, M&A spreads widened to levels last seen during 2008’s Great Financial Crisis, intensified by important deleveraging and platforms closing books in fire sales. The period under review was more calm.

Given the idiosyncratic nature of activist strategies returns were widespread. Overall, given their long bias and tendency of being rather concentrated they managed to greatly participate in the equity markets rally.

Early in the period, merger arbitraging was characterized by tightening spreads and several deals closing, especially larger ones. However, there was an increase in deal breaks and spread widening that hurt certain managers. Following this, spreads continued to tighten and some deals closed successfully. However, with deals closing and new deal flows being inexistent the investable universe shrank meaningfully, forcing managers to take down their gross exposures. Further in the period, there was a pick up in the number of new announced M&A deals and spreads continued to tighten.

Distressed credit managers rebounded nicely from trough, though those with a long and emerging markets bias continue to suffer year-to-date.

MACRO

The first part of the year saw large dispersion across the different sub-strategies. Larger funds underperformed largely.

In the beginning of the period under review, gains were made from rates trading and risk assets long short trading. Traders kept a tactical bias with a possibility to cut risk quickly because of monetary policy uncertainty. Later on, managers generally increased portfolio risks as they want to profit from opportunities ahead. Mid-period, the consensus view was on a weakening USD and more equities tactical trading. Important central banks debt issuance and prolonged near zero-rates has negative implications for rates trading. August’s new Fed policy framework triggered a short term rates sell off and further curve steepening, which managers were positioned to profit from. Macro managers focused on the development of a vaccine and its distribution. They remain confident in that whoever wins the US presidential election will provide more fiscal stimulus.

CTAs entered the period with lower leverage and a defensive positioning, so performance dispersion was rather low. CTAs suffered from FX and commodities trading due to long USD and energy positions which were offset by long equity exposures.

RELATIVE VALUE

The first four months of the year were challenging for relative value strategies, again more for larger funds. Massive cash inflows to overcome a lack of liquidity from central banks helped stabilize the space.

Broadly speaking equity market neutral funds with higher factor risk performed well in this second part of the year. Quantitative funds started with mixed results as investors paid less attention to fundamentals. They were also hurt by beta forecasting errors early June as equities spiked and then quickly sold off. Later, those with low beta factor exposure did well.

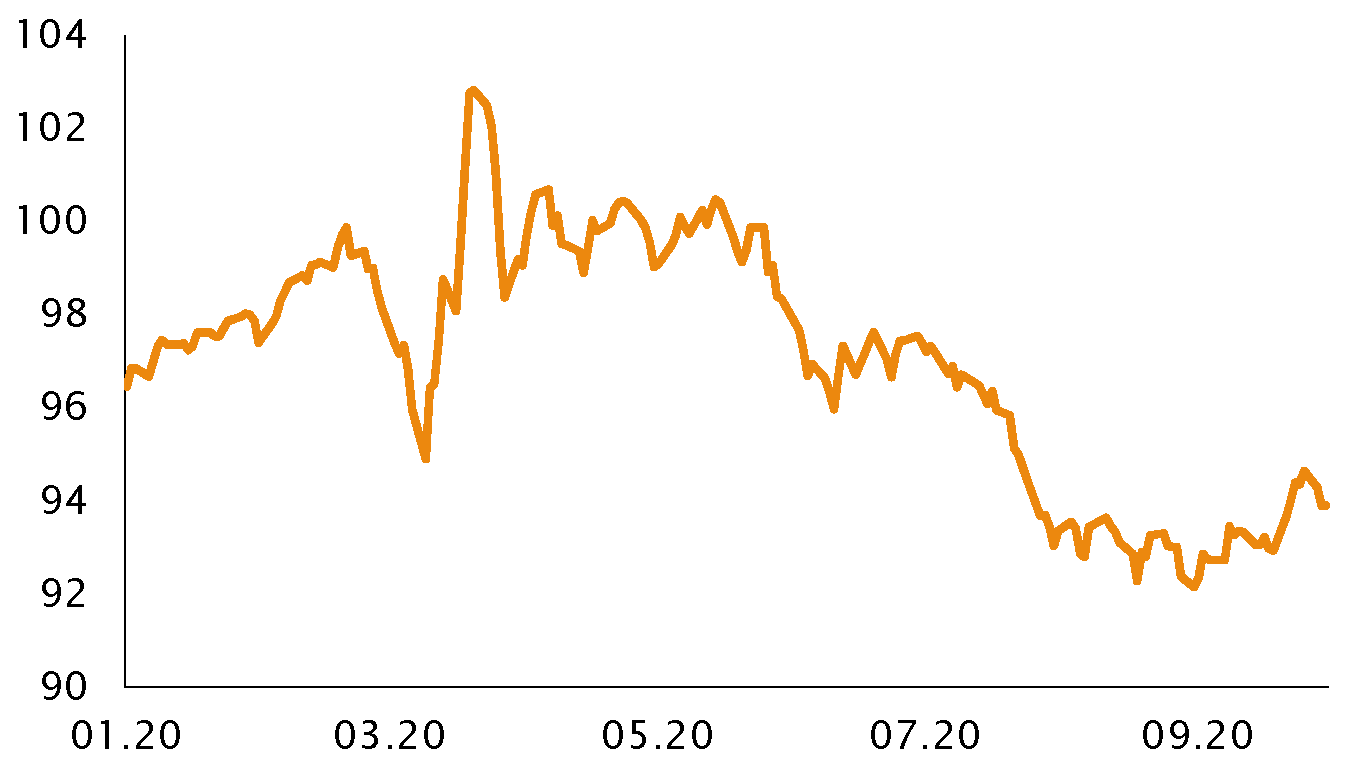

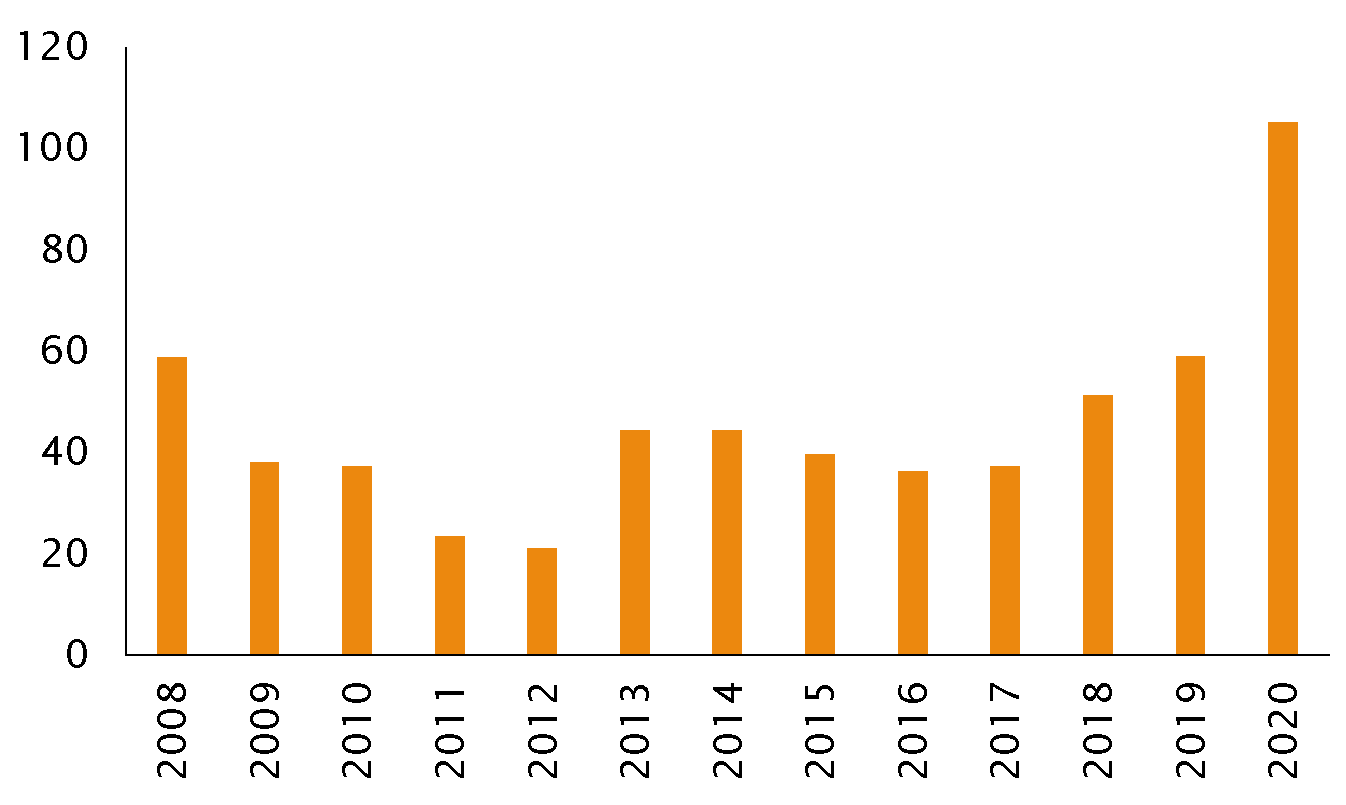

Convertible bonds arbitrageurs profited from two record months for new issuances in May and June. Later on, issuances slowed but remained above usual levels. Throughout the period, they profited from tightening credit spreads.

During the period under review fixed income arbitrageurs generally benefited from a steepening of the yield curve.

Multi-strategy platforms performed well, most sub-strategies contributing positively to performance. Managers added the risk they cut back in March.

OUR CONVICTIONS

At SYZ Capital, we are constantly looking for new sources of alpha to enhance the portfolio diversification. A new strategy emerged within the last few years, namely quantitative credit market neutral. Specialists call it “Scientific fixed income investing”. As we are at an early stage of its development and there are only few players in the field, this strategy has the potential for strong alpha generation, and we think it should last. Its complexity, high setup cost and the experience needed to create algorithms and trading systems make up a high entry barrier for this strategy. Quantitative research on the asset class started over 15 years ago. Its initial purpose was to replicate the same strategy as for equities. However, the bond market is more complex and fragmented. Sufficient access to digital data is recent and continues to grow exponentially along with the breadth of the securities, the market structure and the depth of research necessary to run this strategy.

We are currently aware of only one stand-alone fund in this recently launched strategy. Small allocations, as they are still in development, can be found in multi-strategy quantitative funds. The liquidity of bond markets is not as high as that of equity markets. Therefore, a special attention must be given to an eventual risk of liquidity mismatch and maximum capacity.

We are confident that new stand-alone funds will emerge in the coming years to capture this new source of alpha. On the demand side, the strategy tends to generate uncorrelated returns and therefore should attract investors desperate to find new ways to diversify their portfolios.

Disclaimer

Dieses Werbedokument wurde von der Syz-Gruppe (hierin als «Syz» bezeichnet) erstellt. Es ist nicht zur Verteilung an oder Benutzung durch natürliche oder juristische Personen bestimmt, die Staatsbürger oder Einwohner eines Staats, Landes oder Territoriums sind, in dem die geltenden Gesetze und Bestimmungen dessen Verteilung, Veröffentlichung, Herausgabe oder Benutzung verbieten. Die Benutzer allein sind für die Prüfung verantwortlich, dass ihnen der Bezug der hierin enthaltenen Informationen gesetzlich gestattet ist. Dieses Material ist lediglich zu Informationszwecken bestimmt und darf nicht als ein Angebot oder eine Aufforderung zum Kauf oder Verkauf eines Finanzinstruments oder als ein Vertragsdokument aufgefasst werden. Die in diesem Dokument enthaltenen Angaben sind nicht dazu bestimmt, als Beratung zu Rechts-, Steuer- oder Buchhaltungsfragen zu dienen, und sie sind möglicherweise nicht für alle Anleger geeignet. Die in diesem Dokument enthaltenen Marktbewertungen, Bedingungen und Berechnungen sind lediglich Schätzungen und können ohne Ankündigung geändert werden. Die angegebenen Informationen werden als zuverlässig betrachtet, jedoch übernimmt die Syz-Gruppe keine Garantie für ihre Vollständigkeit oder Richtigkeit. Die Wertentwicklung der Vergangenheit ist keine Garantie für zukünftige Ergebnisse.