Over the last few years, Apple has diversified its products and services while opening up new markets. For example, the leading U.S. smartphone company has established itself in entertainment, launching a subscription-based mobile gaming service (Apple Arcade) and its own streaming platform (Apple TV+). But Apple is also weaving its web in financial services, via the launch of a series of "Fintech" products.

Charles-Henry Monchau

Chief Investment officer

Apple expands its financial services offering

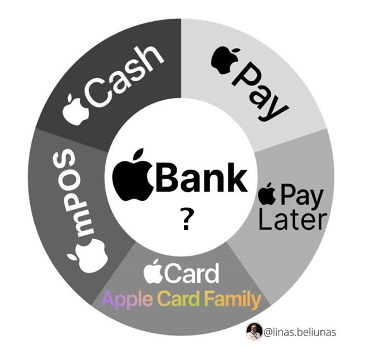

Apple financial services offering

Source

Linas Beliunas

Launched in 2014, Apple Pay is a mobile payment system meant to be an alternative to credit and debit cards. The service allows users to make payments for products and services using Apple's "Near Field Communication" (NFC) technology. A means of payment already widely adopted in China with services such as Alipay and WeChat Pay.

Available since 2019 (and so far only in the U.S.), Apple Card is Apple's "reinvention" of the credit card. The company has partnered with Goldman Sachs as the issuer and Mastercard as the global payment network. The benefits of the card include a wide range of cashback opportunities as well as the absence of a number of fees (late payment, foreign transactions, return payment or annual credit card fees).

Apple mPOS: Launched in early 2022, mobile point of sale or "Tap to Pay" allows merchants to securely accept Apple Pay, contactless cards and other digital wallet payments. App developers and payment platforms can integrate this service into their iOS apps and use it as a payment alternative for their customers.

Apple Cash is a digital card that allows users to send and receive money from the Wallet or Messages apps. Since it is a digital card, Apple Cash can be used for online, in-store and in-app purchases with Apple Pay. Its user-friendly design allows you to make or receive payments and check your balance from Apple Wallet.

About Apple Pay Later

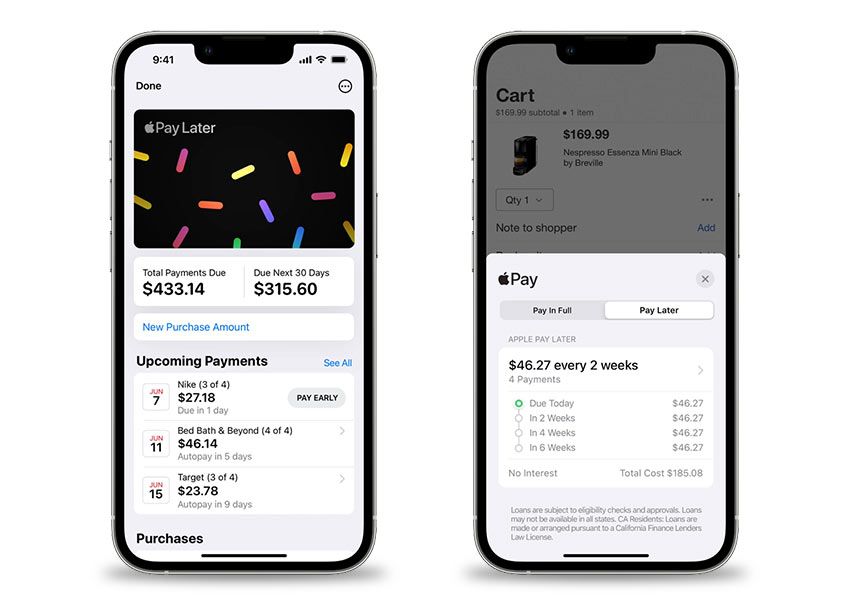

Apple’s latest Fintech service, Apple Pay Later, will be introduced in the second half of this year and will allow users to split a purchase into 4 equal payments over a 6-week period, without interest or fees.

Initially, Apple's "Buy Now, Pay Later" (BNPL) offering will only be available in the United States. Credits will be capped at $1,000, according to CNBC. The service will only be available for online purchases when customers choose to pay with Apple Pay.

Apple is tackling a very competitive market as Apple Pay Later will be no less than the 80th player to enter this segment dominated by Affirm and Klarna. But Apple should benefit from the power of its brand and the influence it has on its consumers. By leveraging its existing customer base (more than 1 billion consumers worldwide, including nearly 200 million in the U.S.), the goal is to seamlessly integrate the service into Apple's portfolio, giving it the largest potential customer base imaginable instantly.

Another competitive advantage for Apple over Klarna, Affirm and other industry players is its self-financing capabilities thanks to its very large cash flow and the considerable cash flows generated every quarter.

An important feature of Apple Pay Later is that qualified consumers already equipped with Apple Pay can apply for Apple Pay Later while in the process of paying for a transaction, whether online or in-store. In practice, this means that a consumer using Apple Pay Later while paying will see the option to pay in four installments appear on their screen. By simply clicking on this option, he/she is instantly enrolled into Apple Pay Later. This feature gives Apple a considerable advantage over existing BNPL players as adoption is made extremely easy.

Note that there will be no credit checks for consumers. By working with Goldman Sachs - its existing partner for Apple Card - Apple has a unique set of data including the payment history of consumers using the Apple Card.

Apple's entry into BNPL offers other benefits to the group. First, it allows Apple to increase its financial gains through BNPL's short-term financing plan. On the other hand, Apple will be able to obtain valuable information about users' purchasing behavior, which will enable it to predict future consumption and spending.

A "home-made" financial service

In the past, Apple has developed its financial services offering by relying on third parties. For example, when Apple developed Apple Card, the firm worked with Goldman Sachs to allow users to have a real bank account on their iPhones.

This time, Apple will gain a lot of autonomy by taking full responsibility for managing the loans made to its customers. A first for the company.

Apple plans to lend from its own balance sheet through a separate company, Apple Financial Services. It will be in charge of checking the background of its customers, granting loans and monitoring repayments.

A development that shows that Apple wants to become less dependent on third-party companies and that even has a name: project "Breakout". So, in addition to loan assessment, Apple could also develop its own payment processing engine. Other functionalities such as customer service, fraud detection or interest rate calculation would be developed by Apple as part of this project.

More Apple financial services could be on the way

According to several experts, Apple should not stop at Apple Pay Later. A service for long-term loans is reportedly in the works. But unlike Apple Pay Later, it could depend on other companies, including Goldman Sachs. In fact, although it is developing its own technologies, Apple reportedly intends to continue working with Goldman and other financial institutions for the Apple Card service and for Apple Pay transactions.

On the other hand, the technologies developed in-house would be used for a future Apple subscription that would allow to pay a monthly fee for having an iPhone. This project had already been mentioned by many sources. And according to the recent Bloomberg article, it is still in the pipeline.

Some experts such as Crone Consulting mention another payment plan project under consideration at Apple: that of a debit card decoupled from financial institutions, i.e.linked to any checking or savings account via the network of automated clearing houses.

Apple has the means to free itself from the financial system. The payment information, plus all the transaction data Apple and Goldman Sachs collect, will allow them to assess the risk of issuing a decoupled debit card, with the help of artificial intelligence. Indeed, the debit card could be the ultimate step in disintermediating financial institutions. And Apple Pay Later is a step that could accelerate that process.

So it would seem that Apple has a real strategy for growth in financial services, as the firm would see these as an indispensable part of its ecosystem of products and services.

For banks and other financial firms, Apple's expansion into this sector is indeed a threat and could potentially impact the growth of new accounts and credit and debit card transactions. As Crone Consulting observes, Apple has designed its new BNPL product as a "preemptive payment." By incorporating the "buy now, pay later" option just before the final payment step, the Apple Pay Later choice appears to be a must-have alternative for consumers, even if their debit or credit cards issued by other financial institutions are stored in their Apple account. In addition, the way Apple Pay Later is tightly integrated with Apple Pay Wallet and Apple Card strengthens Apple's financial ecosystem. The decoupled debit card and other financial services (Trading Apps? Financial advice and products?) could one day expand the offering.

Conclusion

For large technology companies, constant innovation is essential to maintain their leadership. Apple's prospects in smartphones have obviously some limits, so entering the financial sector is an interesting growth opportunity. Indeed, other major technology companies have already ventured into this sector, mainly in Asia, where individuals can use the same device or app to make calls, send text messages, watch videos, make payments and apply for loans.

Within a decade, iPhones have become an extension of the human body. With the iPhone, Apple has built a significant competitive advantage in accessing, processing and leveraging data. It knows the behaviors of its consumers far better than any bank and can leverage that knowledge to offer appropriate and personalized financial products.

Apple's entry into financial services will also give it additional control and information about users, making them increasingly dependent on the interconnected products within the company’s constellation.

Apple's desire to enter this sector has become evident in recent years, with the introduction of Apple Wallet, Apple Card and Apple Pay. The launch of Apple Pay Later is another important step.

Admittedly, there are still barriers to Apple's rise as a financial company. The very strict regulations of the banking industry, as well as the extensive banking expertise that Apple would have to develop in-house are a major obstacle to setting up its own bank. In fact, this is one of the main reasons why large technology companies protect themselves by partnering with banks.

While the company is pursuing this path, it's hard to imagine financial services becoming a major source of revenue or a major part of its business in the short to medium term.

However, Apple will surely continue to diversify its financial services offerings. The profits the company generates each year give it comfortable room to try things in the fintech sector.

Apple is not yet a bank. But the U.S. company seems to be building the means to succeed in financial services and could indeed pose a threat to the sector in the foreseeable future.

Disclaimer

Le présent document a été publié par le Groupe Syz (ci-après dénommé «Syz»). Il n’est pas destiné à être distribué ou utilisé par des personnes physiques ou morales ressortissantes ou résidentes d’un Etat, d’un pays ou d’une juridiction dans lesquels les lois et réglementations en vigueur interdisent sa distribution, sa publication, son émission ou son utilisation. Il appartient aux utilisateurs de vérifier si la Loi les autorise à consulter les informations ci-incluses. Le présent document revêt un caractère purement informatif et ne doit pas être interprété comme une sollicitation ou une offre d’achat ou de vente d’instrument financier quel qu’il soit, ou comme un document contractuel. Les informations qu’il contient ne constituent pas un avis juridique, fiscal ou comptable et peuvent ne pas convenir à tous les investisseurs. Les valorisations de marché, les conditions et les calculs contenus dans le présent document sont des estimations et sont susceptibles de changer sans préavis. Les informations fournies sont réputées fiables. Toutefois, le Groupe Syz ne garantit pas l’exhaustivité ou l’exactitude de ces données. Les performances passées ne sont pas un indicateur des résultats futurs.