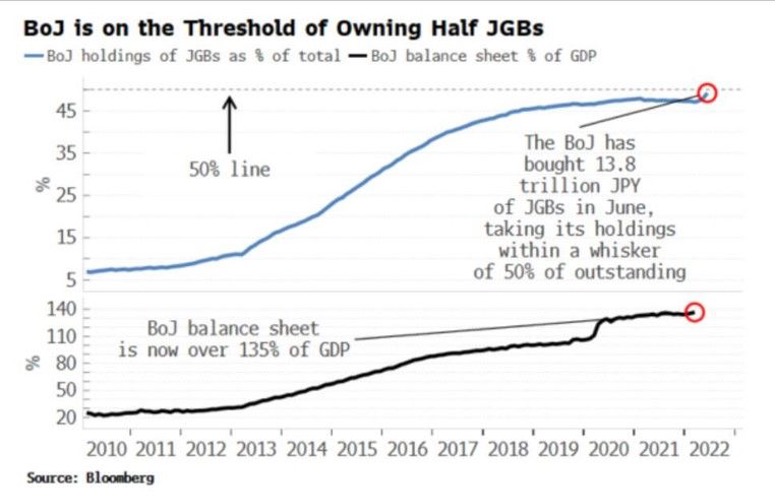

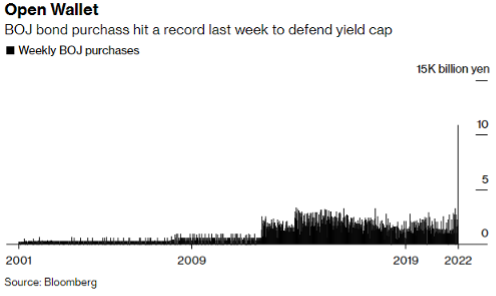

The Bank of Japan’s QE excesses are not without consequences. First, the domestic consequences. By capping the rise in long rates, the BOJ risks pushing inflation well beyond its initial targets. Indeed, the BOJ's bond purchases imply equivalent credit issuance, reinforcing price rises. The yield differential with other developed countries weakens the yen, effectively raising the cost of imported goods and services. The fact that bond yields remain artificially low removes one bulwark against inflation, i.e. the rising cost of credit. The cumulative effect of these factors could create the conditions for inflation to suddenly spiral out of control, implying an inexorable and violent adjustment in the bond market.

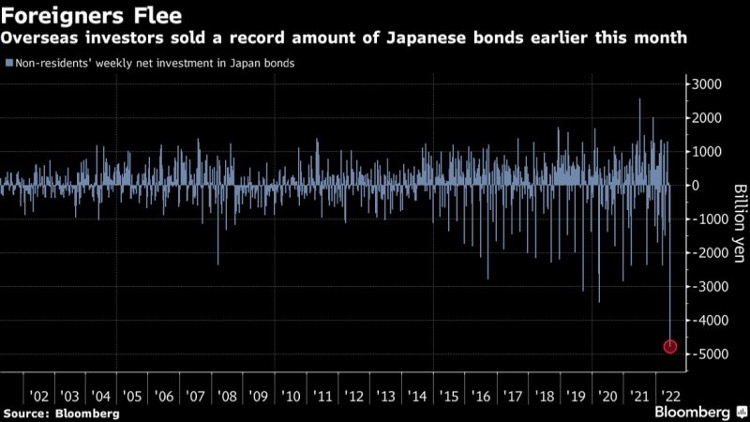

Another corollary of the BOJ's unbridled purchases of JGBs is the risk that the sovereign bond market becomes dysfunctional. Given the astronomical amounts it is buying, the BOJ has created a shortage of government bonds and so has intensified the pressure on domestic financial institutions, causing them to turn to the BOJ for relief. As a result, the central bank is forced to lend the equivalent of the billions of bonds it is buying in the market to avoid a complete paralysis of what was once the world's second deepest bond market.

But Japanese monetary policy also creates many risks on the international stage. The weakening of the yen could lead to a currency war in Asia, which could, in turn, fuel rising inflation in neighbouring countries, increase the cost of servicing their dollar-denominated debts, and so increase the risks of default by less creditworthy countries.

Another international consequence with even greater ramifications is the risk of a sudden unwinding of the carry trade. As mentioned above, the BOJ is obliged to lend the equivalent amount of the bonds it buys. This market context - access to very low-rate financing in a constantly depreciating currency - favours the use of carry trades. For example, a ‘long Brazilian real, short yen’ strategy has already generated gains of 35% this year. But the risk of this type of strategy is a sudden reversal of the trend in place. Indeed, if the yen strengthens and/or if JGB yields rise (due to the BOJ abandoning the YCC), there is a risk of a sudden and massive unwinding of carry trades, with a cascade liquidation of risky assets. This would lead to panic selling of equities, forced selling of the dollar, and a rise in US bond yields (because of the rise in JGB yields). This type of financial accident could effectively worsen the downward movement of risky assets and precipitate a global recession.