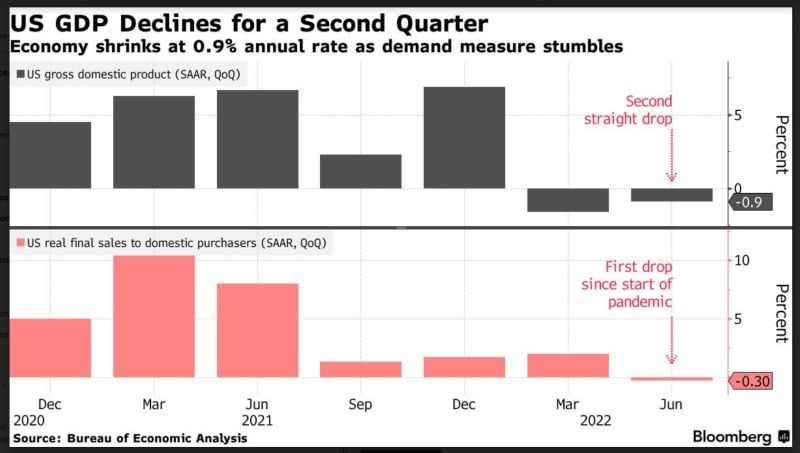

In the space of a few weeks, investors' fears have changed. They are now more focused on the 'r' in recession than the 'r' in rates. The flattening of bond curves, collapse of confidence surveys and GDP figures for the second quarter (published in July) all point to a very clear slowdown in the global economy.

The US is now officially in a technical recession after two quarters of negative GDP growth. Following a 1.6% decline in the first three months of the year, US GDP fell at an annualised rate of 0.9% in the second quarter as inventories and residential investment contributed negatively to growth.