In a nutshell:

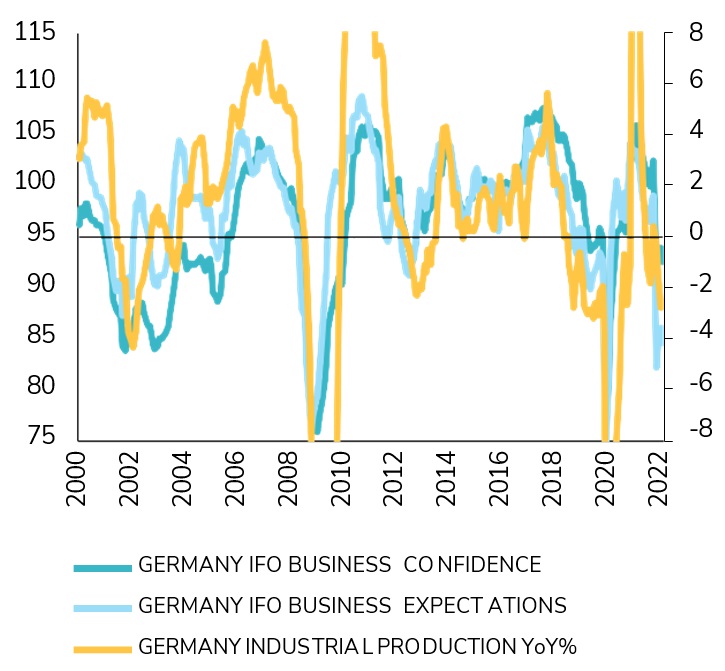

- The macroeconomic landscape of still very elevated inflation projections and declining growth is weighing on risk assets. Markets trade as if recession is imminent. While the US might indeed face a technical recession in the first half of the year, economic indicators and several shock absorbers lead us to think that Uncle Sam can still avoid a full-blown recession. The landscape is different in Europe and will be dependent on Russian gas imports as we exit the summer.

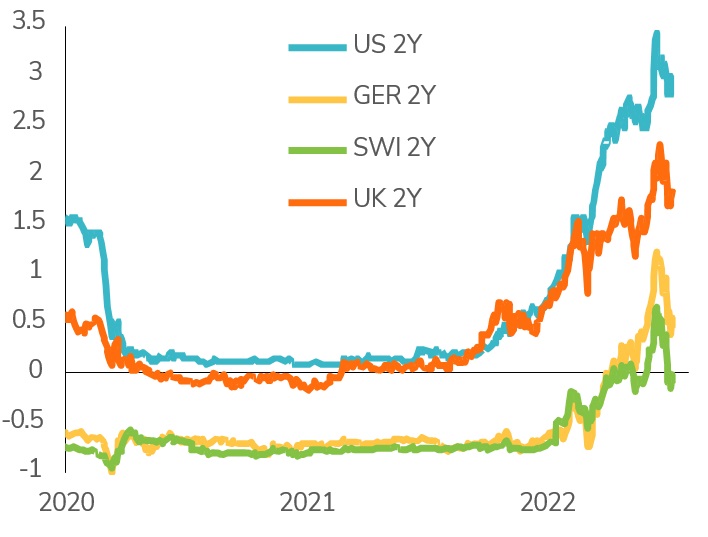

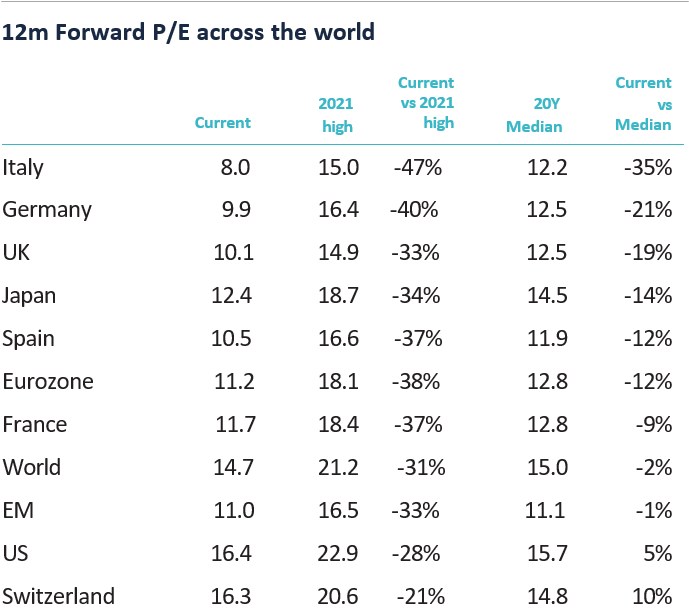

- Liquidity / monetary conditions remain negative as well. For central banks, there is a real risk for inflation to remain high even if growth slows down, forcing them to remain in a tightening mode. Earnings growth has been a tailwind for markets through the first semester but current earnings growth expectations do not reflect the global economic slowdown. We believe that the risk of earnings downgrade is not yet priced in. Valuations were further de-rated but are still not cheap enough.

- Our coincident indicators (market dynamics) are currently positive but can swiftly turn negative, as market instability is high. Trend indicators and market breadth give negative signals while sentiment is oversold but not to the point of triggering a contrarian call.

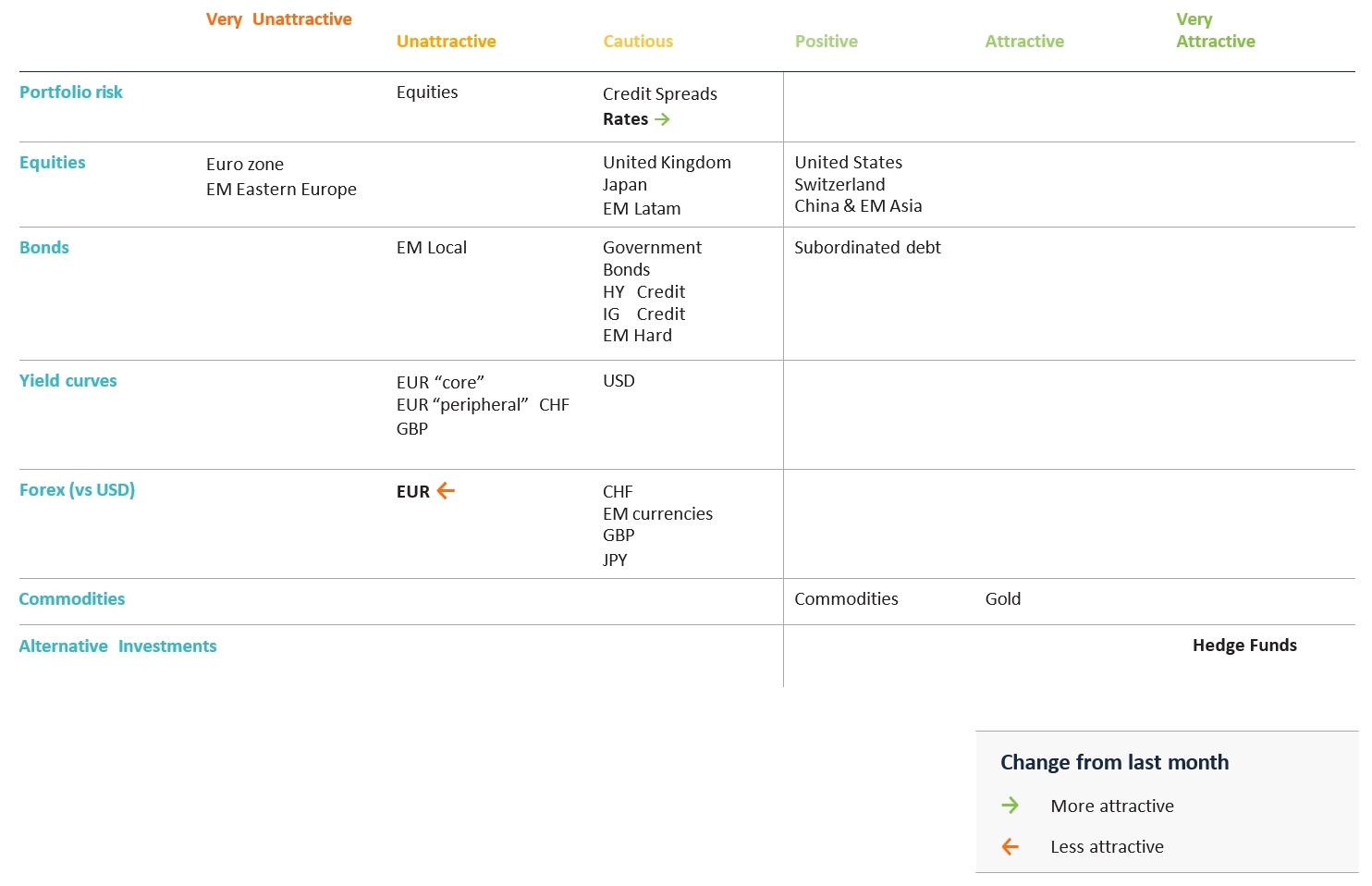

- Overall, the weight of the evidence (i.e. the aggregation of our fundamental and market indicators) remains negative. As such, we maintain an “unattractive” view on equity markets in general. We do a have a positive stance on US, Swiss and China / EM Asia equities. Our least favored markets remains the Eurozone and EM Eastern Europe equities (very unattractive). We maintain a cautious view on the UK, Japan and EM LatAm.

- In Fixed Income, we are upgrading rates from "unattractive" to "cautious" in order to reflect the deteriorating global growth outlook. We keep a "cautious" stance on credit spreads.

- In Forex, we are positive on the dollar against all currencies. We are downgrading the euro one notch further from "cautious" to "unattractive" as the Eurozone is facing a major energy crisis, which is deteriorating the fundamentals of the common currency.

- We keep a positive view on Commodities (with a "preference" stance on Gold) as well as a very attractive view on hedge funds.