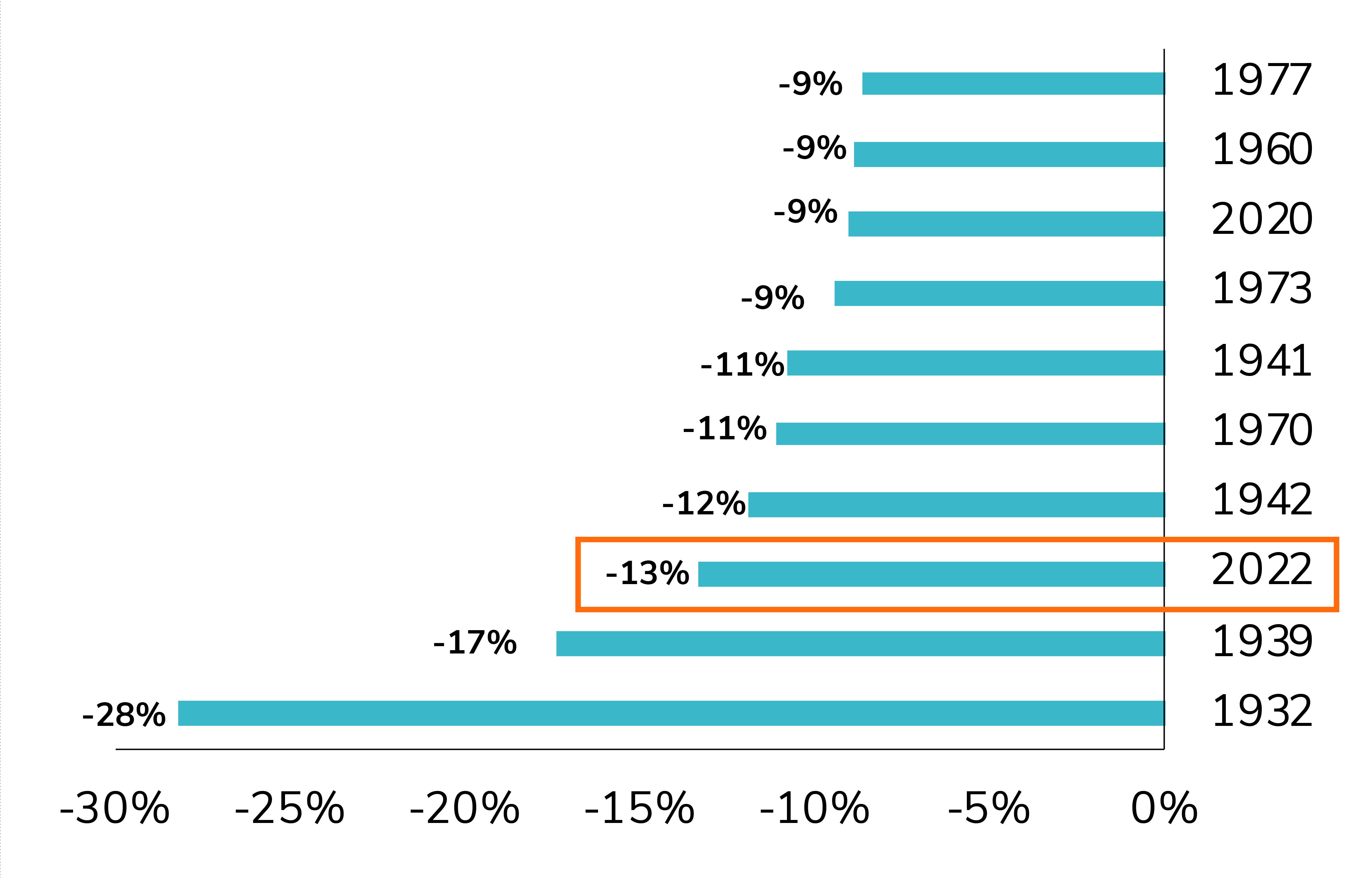

The month of April was a difficult one for risk assets. At the time of our writing, the S&P 500 is down 13.3% year-to-date, its 3rd worst start in history, after 1932 and 1939. Equity markets are currently facing several headwinds:

1. Slowing economic growth: Following a strong rebound in 2021, the global economy is entering a pronounced slowdown amid less favorable conditions with inflation rising, major geopolitical concerns and China’s harsh covid lockdowns;

2. For the first time since more than a decade, central banks are not investor-friendly anymore. The Fed and other central banks have been too slow to tackle inflation and thus need to normalize monetary policy quickly. The hawkish rhetoric and the ensuing increase in bond yields are weighing on equity valuations;

3. Poor visibility on Russia’s war in Ukraine. The longer the war lasts, the longer the sanctions will be in place with negative consequences on commodity supplies and thus further increase risks for inflation.

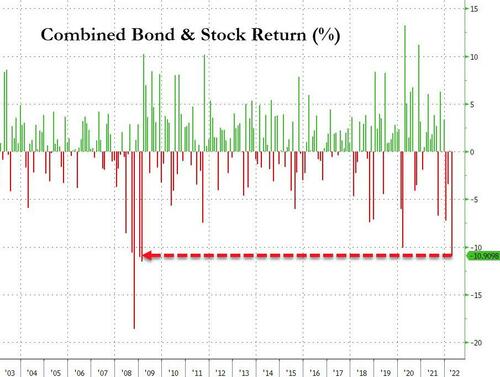

While there are some shock absorbers (healthy consumer & corporate balance sheet, rising earnings, etc.), the market context is definitely less supportive than it has been over the last two years. After a relief rally during the last two weeks of March, the vast majority of equity and bond markets recorded a spike in volatility and negative returns in April.