The Russia-Ukraine conflict has pushed geopolitical risk to a very high level and is having a meaningful impact on global financial markets today through 1/ the rise of equity risk premium; 2/ tighter financial conditions and 3/ higher inflation ahead due to rising energy costs.

We held an extraordinary investment strategy meeting this morning and would like to share our key takeaways below.

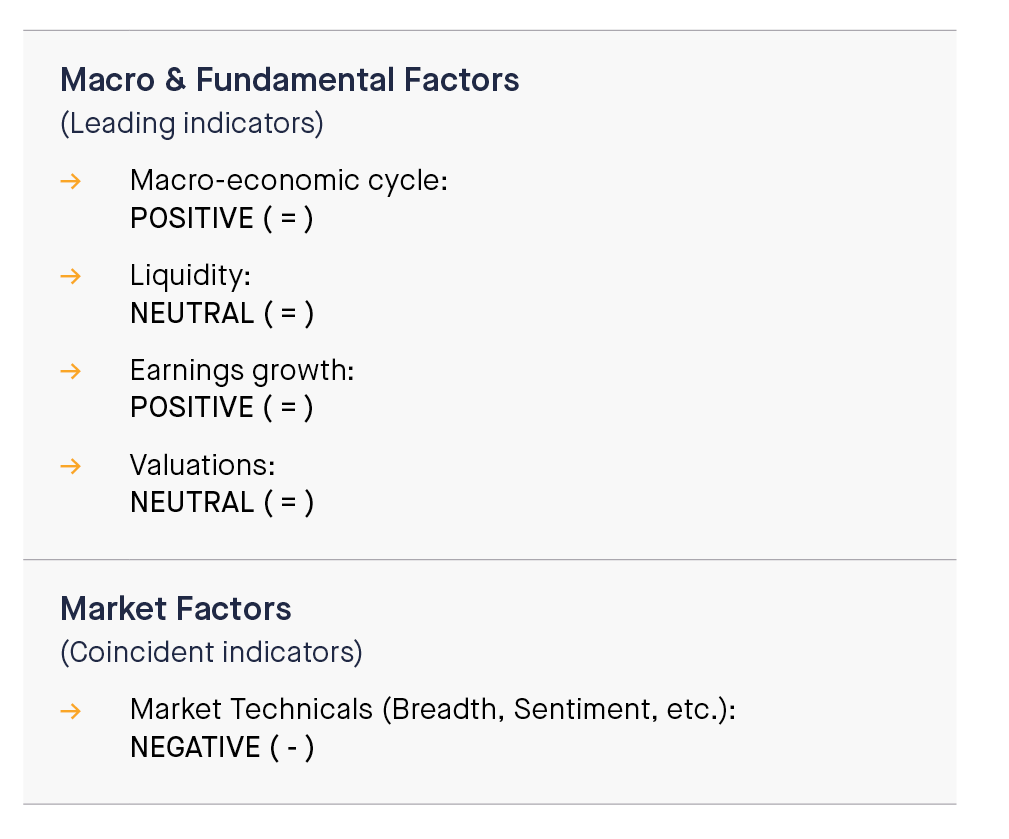

The weight of evidence (i.e the aggregated view of our fundamental & technical indicators) leads us to downgrade our stance on equities from positive to cautious. While global growth remains above potential, the Russia-Ukraine crisis creates downside risk at a time when monetary policy is unlikely to provide a strong support to the economy and financial markets. While earnings growth remains and equity valuations are slightly more attractive, our market technical indicators (trend, sentiment, etc.) have been deteriorating lately and thus lead us to reduce our stance.

An important point: we have been gradually reducing our exposure to equities and credit over the last few months based not only on fundamental & technical indicators but also on systematic risk balancing. This equity reduction comes as further step in this de-risking process.

Key takeaways:

- From a macro perspective, we continue to believe that normalization in growth and inflation rates remains the central scenario for 2022. By “normalization”, we mean that the impact of the post-pandemic recovery on consumption, business investment and supply chains will dissipate and create a fundamentally more normalized economic environment. However, downside risks on growth and upside risks on inflation are clearly increasing for the global economy now, mostly due to the prospect of sustained elevated energy and commodity prices, as well as potential shortages in key raw materials due to sanctions on Russia. ;

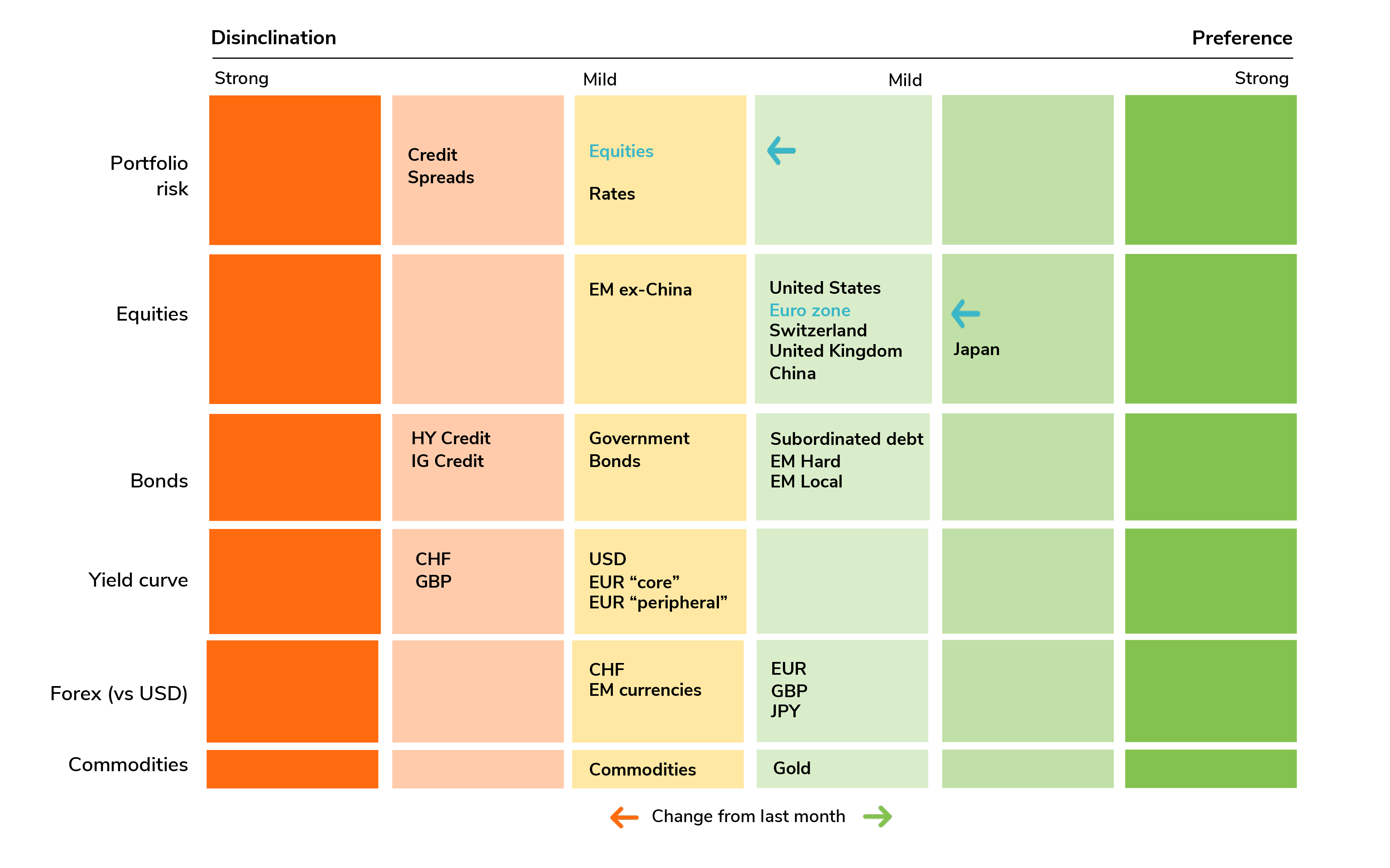

- Equities: from positive to cautious. In the current macro environment of positive economic growth and negative real bond yields, equities remain the most attractive asset class in the medium to long-run. However, our indicators lead us to be cautious in the near-term. We are downgrading our preference for the Eurozone one notch given the higher sensitivity of this region to the current Russia-Ukraine crisis. We keep a preference for Japan, for its attractive valuations and less direct exposure to Russia-Ukraine developments.

- Credit: we keep our disinclination stance. high yield and lower quality investment grade should continue to suffer from declining liquidity, rising interest rates (investors will be less likely to seek lower ratings for high yields) and tight valuations;

- We remain cautious on rates, as the inflation context will prevent central banks from responding as forcefully as in previous crisess with monetary policy easing. Flight to quality increases the attractiveness of “risk free” assets such as US Treasuries and German Bunds but upward pressures on inflation will continue to exert upward pressures on long term rates. Despite market volatility and geopolitical risks, we believe that central banks will roll out their plans to tighten monetary policy conditions;

- In Forex, we remain positive EUR, GBP and JPY against USD given current yield differentials, and cautious on the Swiss Franc and EM currencies. We stay cautious on Commodities and positive on Gold.