Assuming it goes through, the deal will create a global leader in project, engineering and technical services delivery. The industrial logic is compelling given complementary business models and the availability of material cost synergies (>14% of combined 2016E EBITA). It will therefore be significantly earnings enhancing and combined net debt will be $1.6b, implying a manageable 1.9x net debt-to-EBITDA which is then expected to decline to a more appropriate 0.5x -1.5x within 18 months of completion.

Flash

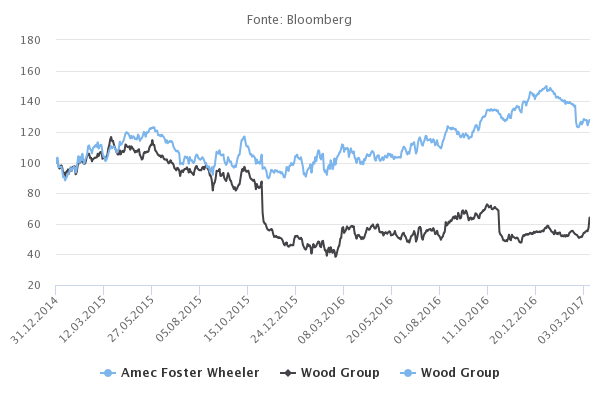

Amec Foster Wheeler to be acquired at a 30% premium by Wood Group

Martedì, 03/14/2017Wood Group surprised the market by announcing an equity-financed bid for Amec Foster Wheeler at a price of 564p, a 28.7% premium to its 3-month average. Although the deal instantly fixes Amec Foster Wheeler’s balance sheet, this wasn’t through the rights issue that we had anticipated. Nonetheless, Wood Group’s shrewd move highlights the longer-term underlying value we identified in Amec Foster Wheeler’s shares.

Michael Clements

European Equities Expert

Alasdair Cummings

Analyst

Given what remains a challenging environment for oil and gas activity, further cost cutting via industry consolidation appears inevitable for the sector.

Strong strategic rationale

Opportunistic timing

Wood Group has a highly successful track record of value creation through well timed acquisitions, and this appears to be another clever deal by the Scots towards the bottom of the cycle. Prior to the bid, Amec Foster Wheeler had underperformed Wood Group by c.70% since 2015, which suggests that now is an attractive time for Wood to make its move. Indeed, the large fall in Amec Foster Wheeler’s share price in November 2015 provided us with the opportunity to initiate a position at ‘bombed-out’ levels. While we do not view the offer price as reflective of Amec Foster Wheeler’s longer-term underlying value, Amec Foster Wheeler shareholders will own 44% of the combined entity which will still enable participation in the turn-around of the company, the significant synergies and scale benefits, and the potential upturn in the cycle.

Counter bid on the cards?

In the wake of the announcement, it would not surprise us if some of the other globally diversified engineering companies were to ‘run the rule’ over Amec Foster Wheeler. Even though Amec Foster Wheeler has recommended the offer, several peers (such as SNC Lavalin, Fluor and Jacobs) have the balance sheet capacity and ability to make compelling cost synergy arguments, which could sway the board to accept a higher rival offer. Given what remains a challenging environment for oil and gas activity, further cost cutting via industry consolidation appears inevitable for the sector.

Disclaimer

Il presente documento di marketing è stato redatto dal Gruppo Syz (di seguito denominato «Syz»). Esso non è destinato alla distribuzione o all’utilizzo da parte di persone fisiche o giuridiche cittadini o residenti in uno Stato, un Paese o una giurisdizione le cui leggi applicabili ne vietino la distribuzione, la pubblicazione, l’emissione o l’utilizzo. Spetta unicamente agli utenti verificare che siano legalmente autorizzati a consultare le informazioni nel presente. Il presente materiale ha esclusivamente finalità informative e non deve essere interpretato come un’offerta o un invito per l’acquisto o la vendita di uno strumento finanziario, o come un documento contrattuale. Le informazioni fornite nel presente non sono intese costituire una consulenza legale, fiscale o contabile e potrebbero non essere adeguate per tutti gli investitori. Le valutazioni di mercato, le durate e i calcoli contenuti nel presente rappresentano unicamente stime e sono soggetti a variazione senza preavviso. Si ritiene che le informazioni fornite siano attendibili; tuttavia, il Gruppo Syz non ne garantisce la completezza o l’esattezza. I rendimenti passati non sono indicativi di risultati futuri.